Nigel Farage calls bank’s apology ‘a start’ but ‘no way near enough’ after account row

Nigel Farage has called on MPs to hold an inquiry into NatWest after one of the group’s banks, Coutts, closed his account.

The former UKIP and Brexit Party leader has claimed the elite bank took the action because his views did not align with the firm’s “values”.

But other media reports suggested it was down to his finances not reaching the company’s threshold, and Coutts insisted it did not close accounts “solely on the basis of legally held political and personal views”.

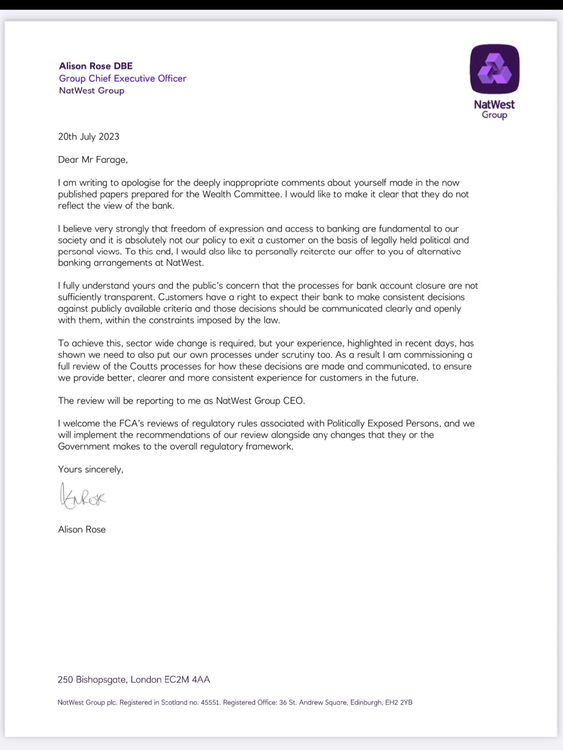

Earlier, the chief executive officer of NatWest, Alison Rose, wrote to Mr Farage offering him an apology, after he claimed to have a 40-page document that proved Coutts “exited” him because he was regarded as “xenophobic and racist” and a former “fascist”.

In the letter, she said “deeply inappropriate comments” had been made about him in documents prepared for the company’s wealth committee, and the remarks “did not reflect the view of the bank”.

She added: “I believe very strongly that freedom of expression and access to banking are fundamental to our society and it is absolutely not our policy to exit a customer on the basis of legally held political and personal views.”

The bank has now offered “alternative banking arrangements” at NatWest.

Speaking to reporters on Thursday night, Mr Farage called the apology “a start, but it is no way near enough”.

“It is always good to get an apology, particularly from somebody running a bank with 19 million customers, so thank you for the apology,” he added. “But it does feel ever so slightly forced.

“It also felt a bit like, ‘not me guv’.”

The apology letter written to Nigel Farage

The letter came as the Treasury announced new stricter measures on banks closing accounts to protect freedom of expression.

The government said the organisations will now have to inform customers of the reasons why they are closing accounts, and extend the notice period from 30 days to 90 – giving customers more time to challenge the decision or find a new bank.

Economic Secretary to the Treasury, Andrew Griffith, said: “Freedom of speech is a cornerstone of our democracy, and it must be respected by all institutions.

“Banks occupy a privileged place in society, and it is right that we fairly balance the rights of banks to act in their commercial interest, with the right for everyone to express themselves freely.”

Mr Farage praised the “superb” and “rapid reaction” of the government. But he also claimed his apology from Ms Rose only came about due to pressure from the Treasury.

The now-TV presenter added that wanted to know “what was said at a dinner” between Ms Rose and a BBC journalist.

Sky News has contacted Coutts and Mr Farage for comment.

Asked if he did have enough money to hold an account with Coutts, whose website states clients are “required to maintain at least £1m in investments or borrowing [mortgage], or £3m in savings”, Mr Farage said: “I have been a customer of the group for 43 years, I have been a customer of Coutts since 2014. At no point did anybody say you have to have this amount of money.

“These things are all discretionary [and] they were using this, frankly, as a mask to cover up the truth.

“This is not about money in the account, this is about the fact they don’t like me.”

Asked if he thought Ms Rose should resign, Mr Farage added: “I think rather than just saying right now [Ms Rose] ought to go, I think now what needs to happen is the Treasury Select Committee needs to reconvene, come out of recess, and lets give her the opportunity to tell us the truth.”

Read more:

What happened to Nigel Farage’s bank account?

Are banks allowed to close accounts?

Farage: ‘I was shocked with the vitriol’

In her letter, Ms Rose said she “fully understands” both Mr Farage’s and the public’s concerns that the processes for bank account closures were not “sufficiently transparent”, adding: “Customers have a right to expect their bank to make consistent decisions against publicly available criteria and those decisions should be communicated clearly and openly with them, within the constraints imposed by the law.”

She agreed that “sector-wide change” was needed but, following the incident with Mr Farage and Coutts, she would now commission a full review of the bank’s processes “to ensure we provide better, clearer and more consistent experience for customers in the future”.

In a further statement released after Sky News broke the story of the letter, Ms Rose reiterated her apology, but added: “It is not our policy to exit a customer on the basis of legally held political and personal views.

“Decisions to close an account are not taken lightly and involve a number of factors including commercial viability, reputational considerations, and legal and regulatory requirements.”

Rachel Reeves has said she is determined to “defy” forecasts that suggest she will face a multibillion-pound black hole in next month’s budget.

Writing in The Guardian, the chancellor argued the “foundations of Britain’s economy remain strong” – and rejected claims the country is in a permanent state of decline.

Reports have suggested the Office for Budget Responsibility is expected to downgrade its productivity growth forecast by about 0.3 percentage points.

Rachel Reeves. PA file pic

That means the Treasury will take in less tax than expected over the coming years – and this could leave a gap of up to £40bn in the country’s finances.

Ms Reeves wrote she would not “pre-empt” these forecasts, and her job “is not to relitigate the past or let past mistakes determine our future”.

“I am determined that we don’t simply accept the forecasts, but we defy them, as we already have this year. To do so means taking necessary choices today, including at the budget next month,” the chancellor added.

She also pointed to five interest rate cuts, three trade deals with major economies and wages outpacing inflation as evidence Labour has made progress since the election.

Speculation is growing that Ms Reeves may break a key manifesto pledge by raising income tax or national insurance during the budget on 26 November.

Read more from Sky News:

What tax rises and spending cuts could Reeves announce?

Start-ups warn the chancellor over budget tax bombshell

Chancellor faces tough budget choices

Although her article didn’t address this, she admitted “our country and our economy continue to face challenges”.

Her opinion piece said: “The decisions I will take at the budget don’t come for free, and they are not easy – but they are the right, fair and necessary choices.”

Yesterday, Sky’s deputy political editor Sam Coates reported that Ms Reeves is unlikely to raise the basic rates of income tax or national insurance, to avoid breaking a promise to protect “working people” in the budget.

Tax hikes possible, Reeves tells Sky News

Sky News has also obtained an internal definition of “working people” used by the Treasury, which relates to Britons who earn less than £45,000 a year.

This, in theory, means those on higher salaries could be the ones to face a squeeze in the budget – with the Treasury stating that it does not comment on tax measures.

Read more: The taxes Reeves could raise

In other developments, some top economists have warned Ms Reeves that increasing income tax or reducing public spending is her only option for balancing the books.

Experts from the Institute for Fiscal Studies have cautioned the chancellor against opting to hike alternative taxes instead, telling The Independent this would “cause unnecessary amounts of economic damage”.

Although such an approach would help the chancellor avoid breaking Labour’s manifesto pledge, it is feared a series of smaller changes would make the tax system “ever more complicated and less efficient”.

KitKats, Gaviscon, toothpaste, and even Freddo have all fallen victim to shrinkflation, consumer group Which? has found.

As families struggle with the cost of a trip to the supermarket, a survey of shoppers revealed how many products are getting smaller – while others are being downgraded with cheaper ingredients.

Among the examples are:

• Aquafresh complete care original toothpaste – from £1.30 for 100ml to £2 for 75ml at Tesco, Sainsbury’s and Ocado

• Gaviscon heartburn and indigestion liquid – from £14 for 600ml to £14 for 500ml at Sainsbury’s

• Sainsbury’s Scottish oats – from £1.25 for 1kg to £2.10 for 500g

• KitKat two-finger multipacks – from £3.60 for 21 bars to £5.50 for 18 bars at Ocado

• Quality Street tubs – from £6 for 600g to £7 for 550g at Morrisons

• Freddo multipacks – from £1.40 for five bars to £1.40 for four bars at Morrisons, Ocado and Tesco

Which? also received reports of popular treats missing key ingredients, as manufacturers seek to cut costs.

The amount of cocoa butter in white KitKats has fallen below 20%, meaning they can no longer actually be sold as white chocolate.

It comes after Penguin and Club bars lost their legal status as a chocolate biscuit, as they now contain more palm oil and shea oil than cocoa – as reported in the Sky News Money blog.

Which? retail editor Reena Sewraz called on supermarkets to be “more upfront” about price changes to help households “already under immense financial pressure” get better value.

While keeping track of the size and weight of products can be tricky, Which? has two top tips for detecting shrinkflation.

The first is to be wary of familiar products labelled as “new” – because the only thing that’s new may end up being the smaller size.

Meanwhile, the second is to pay attention to how much an item costs per 100g or 100ml, as this can be an easy way of finding out when prices change.

What have the companies said?

A spokeswoman for Mondelez International, which makes Cadbury products, said any change to product sizes are a “last resort”, but it’s facing “significantly higher input costs across our supply chain” – including for energy.

A Nestle spokesman said it was seeing “significant increases in the cost of coffee”, and some “adjustments” were occasionally needed “to maintain the same high quality and delicious taste that consumers know and love”.

“Retail pricing is always at the discretion of individual retailers,” they added.

A spokesman for the Food and Drink Federation also pointed to government policy, notably national insurance increases for employers and a new packaging tax.

Is inflation reaching its peak?

Fresh food prices on the rise

The Which? report comes as latest figures showed fresh food costs 4.3% more than it did a year ago.

The increase in October, reported by the British Retail Consortium (BRC) and market researchers NIQ, was up on the 4.1% year-on-year rise in September.

Overall food inflation was down slightly, though, to 3.7% from last month’s 4.2%.

Read more from Sky News:

Surprise move for Costa Coffee

Start-ups issue warning to Reeves

There has also been a slowdown in overall shop price inflation, which the BRC said was down to “fierce competition among retailers” ahead of Black Friday sales.

The annual shopping extravaganza will this year arrive in the same week as the chancellor’s budget, which is set for Wednesday 26 November.

BRC chief executive Helen Dickinson called on Rachel Reeves to help “relieve some pressures” keeping prices high, with the national insurance rise in last year’s budget having “directly contributed to rising inflation”.

“Adding further taxes on retail businesses would inevitably keep inflation higher for longer,” Ms Dickinson warned.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024