From tuition to takeaways, why China’s regulatory crackdown is proving unappetising for investors

China’s government has just provided investors with another reminder of why they should tread carefully when putting money into the country.

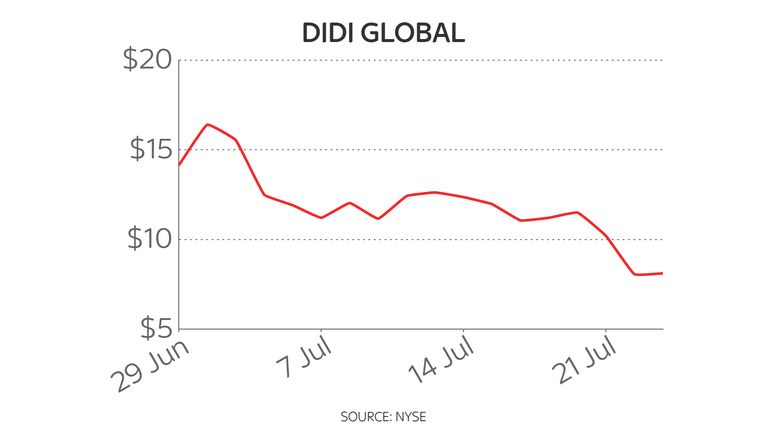

At the end of last month, the Chinese ride-hailing app Didi made history when it floated on the New York Stock Exchange with a valuation of $70bn, making it the biggest IPO of a Chinese company in seven years.

Just days later, the Chinese government told Didi to stop registering new drivers and users for its app, which it followed by demanding that Didi be removed from Chinese app stores.

Didi was targeted days after floating in New York

The shares plunged and are now 42% lower than the price at which they listed.

Now Beijing has done it again with a fresh salvo aimed at tech and education companies.

Firstly, the Chinese government announced on Friday night that it was banning private tutoring and test preparation for core school subjects, arguing the move would ease financial pressure on hard-up Chinese families.

Private tutoring in China is a $120billion-a-year business and around three-quarters of Chinese children are reckoned to have some form of private tuition outside school.

Beijing, which is concerned about the country’s rapidly-ageing population, suspects the financial pressure of educating children privately may be a reason why couples are still not having more children despite the abolition in 2015 of the “one child” policy.

The measure, which is believed to have come from President Xi Jinping himself, was accompanied by restrictions on foreign investment in private tutoring companies and is also expected to see advertising bans imposed – as well as restrictions on when tutoring can be made available.

The clampdown on tutoring is believed to have come from President Xi Jinping himself. Pic: AP

The move sent shares of private tuition companies, many of which are listed in Hong Kong, tumbling.

New Oriental Education & Technology finished the session down 47%, while Scholar Education fell by 45% and Koolearn Technology by 33%.

Next came an attack on Tencent, one of China’s biggest tech companies, which on Saturday was ordered to give up the exclusive music licensing agreements it has signed with record companies – including Universal Music and Warner Music – around the world.

Tencent, which owns China’s most popular messaging service WeChat, is estimated to have an 80% share of the exclusive music streaming market in the country.

Shares of Tencent fell by almost 8% on the news.

Then, Beijing unveiled measures aimed at cooling what it sees as an overheated property market.

The People’s Bank of China (PBoC) is reported to have ordered lenders to raise mortgage rates for first time buyers from 4.65% to 5%.

At the same time, the PBoC is said to have ordered an increase in the interest rate for people buying second homes from 5.25% to 5.7%. That sent shares in property development companies lower.

Private tuition is big business for companies such as Koolearn Pic: AP

Separately, China also today announced new rules aimed at better protecting delivery riders, following complaints that some are not being paid the minimum wage or are being sent on routes where it is impossible to complete the order in the time allowed.

That news sent shares of Meituan, one of China’s biggest food delivery companies, down by 14%.

Its shares have now halved in value since February.

Shares of the e-commerce giant Alibaba, which also operates a popular delivery service called Ele.me, fell by more than 6%.

Taken together, the various measures add up to an unappetising cocktail for investors, who reacted accordingly.

In Hong Kong, the Hang Seng slid by 4.13%, taking it to a level not seen since December last year.

In Shanghai, the blue-chip CSI300 index fell by 3.22%, again wiping out all gains for the year to date.

The broader Shanghai Composite, meanwhile, fell by 2.34% to a two-month low.

Didi’s shares are now lower than the price at which they listed

There are two schools of thought as to what Beijing is doing here.

One is that this is just part of a wider campaign by the Chinese Communist Party to reassert its influence over life in China and strengthen its hand – with businesses and investors merely being caught up in this.

The other argues that this is a specific set of measures aimed at clipping the wings of businesses amid concerns that too many of them are not always operating within the law.

Aside from complaints about the treatment of workers in delivery firms, there is also a sense that the accounting practices of some property companies many not stand up to scrutiny, that the banks are being too lax with their lending standards and that the wealth being created by some of these companies, particularly those in the tech sector, are being too concentrated among a handful of plutocrats.

That theory is given credence by, for example, the way Beijing scuppered last year’s proposed stock market flotation of the payments company Ant Financial, which would have further added to the wealth of Jack Ma, the billionaire entrepreneur that created Ant and its former parent company, Alibaba.

Concerns about the quality of accounting at some companies have been rumbling ever since a former stock market darling, the coffee shop operator Luckin Coffee, collapsed last year after falsifying its accounts.

Either way, investors have been spooked, although some will have only themselves to blame given the way regulatory risk in China has been overlooked in recent years.

But it has certainly prompted investors in China to look more closely at their portfolios as they try to assess what other companies are at risk of seeing their business models reduced to rubble overnight by regulators.

Rightly so.

This Chinese government is very different from its immediate predecessors and is clearly far more relaxed about alienating foreign investors if it considers more important principles are at stake.

The UK economy unexpectedly shrank in May, even after the worst of Donald Trump’s tariffs were paused, official figures showed.

A standard measure of economic growth, gross domestic product (GDP), contracted 0.1% in May, according to the Office for National Statistics (ONS).

Rather than a fall being anticipated, growth of 0.1% was forecast by economists polled by Reuters as big falls in production and construction were seen.

It followed a 0.3% contraction in April, when Mr Trump announced his country-specific tariffs and sparked a global trade war.

A 90-day pause on these import taxes, which has been extended, allowed more normality to resume.

This was borne out by other figures released by the ONS on Friday.

Exports to the United States rose £300m but “remained relatively low” following a “substantial decrease” in April, the data said.

Overall, there was a “large rise in goods imports and a fall in goods exports”.

A ‘disappointing’ but mixed picture

It’s “disappointing” news, Chancellor Rachel Reeves said. She and the government as a whole have repeatedly said growing the economy was their number one priority.

“I am determined to kickstart economic growth and deliver on that promise”, she added.

But the picture was not all bad.

Growth recorded in March was revised upwards, further indicating that companies invested to prepare for tariffs. Rather than GDP of 0.2%, the ONS said on Friday the figure was actually 0.4%.

It showed businesses moved forward activity to be ready for the extra taxes. Businesses were hit with higher employer national insurance contributions in April.

Read more:

Trump plans to hit Canada with 35% tariff – warning of blanket hike for other countries

Woman and three teenagers arrested over M&S, Co-op and Harrods cyber attacks

The expansion in March means the economy still grew when the three months are looked at together.

While an interest rate cut in August had already been expected, investors upped their bets of a 0.25 percentage point fall in the Bank of England’s base interest rate.

Such a cut would bring down the rate to 4% and make borrowing cheaper.

Is Britain going bankrupt?

Analysts from economic research firm Pantheon Macro said the data was not as bad as it looked.

“The size of the manufacturing drop looks erratic to us and should partly unwind… There are signs that GDP growth can rebound in June”, said Pantheon’s chief UK economist, Rob Wood.

Why did the economy shrink?

The drops in manufacturing came mostly due to slowed car-making, less oil and gas extraction and the pharmaceutical industry.

The fall was not larger because the services industry – the largest part of the economy – expanded, with law firms and computer programmers having a good month.

It made up for a “very weak” month for retailers, the ONS said.

Monthly Gross Domestic Product (GDP) figures are volatile and, on their own, don’t tell us much.

However, the picture emerging a year since the election of the Labour government is not hugely comforting.

This is a government that promised to turbocharge economic growth, the key to improving livelihoods and the public finances. Instead, the economy is mainly flatlining.

Output shrank in May by 0.1%. That followed a 0.3% drop in April.

Ministers were celebrating a few months ago as data showed the economy grew by 0.7% in the first quarter.

Hangover from artificial growth

However, the subsequent data has shown us that much of that growth was artificial, with businesses racing to get orders out of the door to beat the possible introduction of tariffs. Property transactions were also brought forward to beat stamp duty changes.

Read more:

Trump to hit Canada with 35% tariff

Woman and three teens arrested over cyber attacks

In April, we experienced the hangover as orders and industrial output dropped. Services also struggled as demand for legal and conveyancing services dropped after the stamp duty changes.

Many of those distortions have now been smoothed out, but the manufacturing sector still struggled in May.

Signs of recovery

Manufacturing output fell by 1% in May, but more up-to-date data suggests the sector is recovering.

“We expect both cars and pharma output to improve as the UK-US trade deal comes into force and the volatility unwinds,” economists at Pantheon Macroeconomics said.

Meanwhile, the services sector eked out growth of 0.1%.

A 2.7% month-to-month fall in retail sales suppressed growth in the sector, but that should improve with hot weather likely to boost demand at restaurants and pubs.

Struggles ahead

It is unlikely, however, to massively shift the dial for the economy, the kind of shift the Labour government has promised and needs in order to give it some breathing room against its fiscal rules.

The economy remains fragile, and there are risks and traps lurking around the corner.

Is Britain going bankrupt?

Concerns that the chancellor, Rachel Reeves, is considering tax hikes could weigh on consumer confidence, at a time when businesses are already scaling back hiring because of national insurance tax hikes.

Inflation is also expected to climb in the second half of the year, further weighing on consumers and businesses.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike