Kwasi Kwarteng to hold meeting with bankers as fallout from mini-budget continues

Chancellor Kwasi Kwarteng is due to meet bankers today in an effort to calm nerves after his mini-budget spooked the markets and sent the pound crashing.

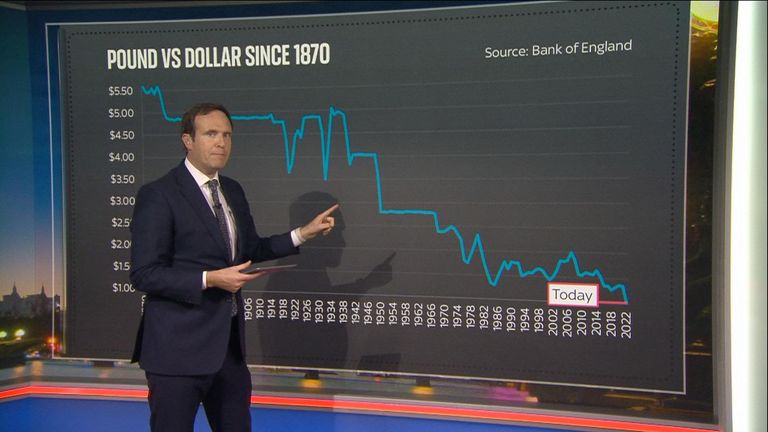

Sky News understands he will ask financiers not to bet against the pound, which has fallen to record lows against the dollar in recent days.

He is also expected to underline his commitment to fiscal discipline and will talk about a “Big Bang 2.0 event” from his growth plan.

Politics live: Kwarteng holds call with nervous Tory MPs

The government has denied he will be asking bankers not to short the pound.

The chancellor is facing international pressure to change course after he unveiled the biggest programme of tax cuts for 50 years in his mini-budget last Friday.

In an extraordinary statement on Tuesday, the International Monetary Fund (IMF) said it was “closely monitoring” developments in the UK and urged Mr Kwarteng to “re-evaluate the tax measures”.

It said that the plans, including the abolition of the 45p rate of income tax for people earning more than £150,000, are likely to increase inequality.

The Bank of England (BoE) has signalled it was ready to significantly ramp up interest rates to shore up the pound and guard against increased inflation.

The chancellor has insisted he is “confident” his strategy will deliver the promised economic growth.

Last night he spoke by phone to Tory MPs at a time of growing anger on the backbenches over the government’s strategy.

IMF hits out at mini-budget – live updates.

Some have been openly expressing concerns about the new economic approach, and the effect it has had on financial markets, saying the party risks trashing its reputation for managing the economy with voters.

Veteran Conservative MP Sir Roger Gale says that another financial crash may be on the way.

Speaking to Good Morning Britain, he said the situation amounts to a “perfect storm”.

He added: “I’m sadly old enough to remember the last financial crash.

“When… people would come into the surgery in tears because they were losing homes and they were losing businesses.

“It was not a pretty sight and I don’t want to see it happen again.”

Chancellor defends budget in phone call with Tory MPs

Sky News understands that the chancellor stood by his decision to cut taxes for the highest earners on his call yesterday, telling MPs “it was a tough choice but the right choice”.

Sky’s economics and data editor Ed Conway takes a look at the most recent numbers on the pound’s volatility.

Read More:

More mortgage providers pull deals over rate rise fears

‘End of NHS’ if chancellor doesn’t reverse mini-budget

He argued his fiscal strategy was focused on the medium-term, and was aimed at showing voters “we can be more efficient in how we spend taxpayers’ money”.

He went on to say that the economic situation would be better in 2024, before what he said was always going to be a “tricky” general election – with Labour currently surging ahead in the polls.

He told MPs that he was establishing a “good working relationship” with the governor of the Bank of England and was in daily contact with him.

He also acknowledged that markets had been volatile but said they were now “settling down” and argued the turmoil reflected a frustration that the markets had not known everything that was included in the mini-budget.

The cyber attack on Jaguar Land Rover (JLR), which halted production for nearly six weeks at its sites, cost the company roughly £200m, it has been revealed.

Latest accounts released on Friday showed “cyber-related costs” were £196m, which does not include the fall in sales.

Profits took a nose dive, falling from nearly £400m (£398m) a year ago to a loss of £485m in the three months to the end of September.

Money blog: Apple launches £220 iPhone ‘sock’ today – fans are divided

Revenues dropped nearly 25% and the effects may continue as the manufacturing halt could slow sales in the final three months of the year, executives said.

The impact of the shutdown also hit factories across the car-making supply chain.

Slowing the UK economy

The production pause was a large contributor to a contraction in UK economic growth in September, official figures showed.

Had car output not fallen 28.6%, the UK economy would have grown by 0.1% during the month. Instead, it fell by 0.1%.

How cyber attack ‘effectively hacked GDP’

Read more from Sky News:

Telegraph future in limbo again as RedBird abandons £500m deal

Reacting to JLR’s impact on the GDP contraction, its chief financial officer, Richard Molyneux, said it was “interesting to hear” and it “goes to reinforce” that JLR is really important in the UK economy.

The company, he said, is the “biggest exporter of goods in the entire country” and the effect on GDP “is a reflection of the success JLR has had in past years”.

Recovery

The company said operations were “pretty much back running as normal” and plants were “at or approaching capacity”.

Production of all luxury vehicles resumed.

Investigations are underway into the attack, with law enforcement in “many jurisdictions” involved, the company said.

When asked about the cause of the hack and the hackers, JLR said it was not in a position to answer questions due to the live investigation.

A run of attacks

The manufacturer was just one of a number of major companies to be seriously impacted by cyber criminals in recent months.

Are we in a cyber attack ‘epidemic’?

High street retailer Marks and Spencer estimated the cost of its IT outage was roughly £136m. The sum only covers the cost of immediate incident systems response and recovery, as well as specialist legal and professional services support.

The Co-Op and Harrods also suffered service disruption caused by cyber attacks.

Four people were arrested by police investigating the incidents.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024