Kwasi Kwarteng to hold meeting with bankers as fallout from mini-budget continues

Chancellor Kwasi Kwarteng is due to meet bankers today in an effort to calm nerves after his mini-budget spooked the markets and sent the pound crashing.

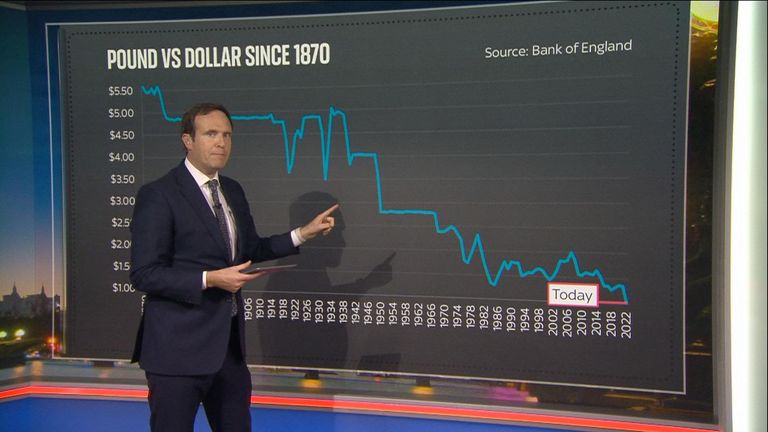

Sky News understands he will ask financiers not to bet against the pound, which has fallen to record lows against the dollar in recent days.

He is also expected to underline his commitment to fiscal discipline and will talk about a “Big Bang 2.0 event” from his growth plan.

Politics live: Kwarteng holds call with nervous Tory MPs

The government has denied he will be asking bankers not to short the pound.

The chancellor is facing international pressure to change course after he unveiled the biggest programme of tax cuts for 50 years in his mini-budget last Friday.

In an extraordinary statement on Tuesday, the International Monetary Fund (IMF) said it was “closely monitoring” developments in the UK and urged Mr Kwarteng to “re-evaluate the tax measures”.

It said that the plans, including the abolition of the 45p rate of income tax for people earning more than £150,000, are likely to increase inequality.

The Bank of England (BoE) has signalled it was ready to significantly ramp up interest rates to shore up the pound and guard against increased inflation.

The chancellor has insisted he is “confident” his strategy will deliver the promised economic growth.

Last night he spoke by phone to Tory MPs at a time of growing anger on the backbenches over the government’s strategy.

IMF hits out at mini-budget – live updates.

Some have been openly expressing concerns about the new economic approach, and the effect it has had on financial markets, saying the party risks trashing its reputation for managing the economy with voters.

Veteran Conservative MP Sir Roger Gale says that another financial crash may be on the way.

Speaking to Good Morning Britain, he said the situation amounts to a “perfect storm”.

He added: “I’m sadly old enough to remember the last financial crash.

“When… people would come into the surgery in tears because they were losing homes and they were losing businesses.

“It was not a pretty sight and I don’t want to see it happen again.”

Chancellor defends budget in phone call with Tory MPs

Sky News understands that the chancellor stood by his decision to cut taxes for the highest earners on his call yesterday, telling MPs “it was a tough choice but the right choice”.

Sky’s economics and data editor Ed Conway takes a look at the most recent numbers on the pound’s volatility.

Read More:

More mortgage providers pull deals over rate rise fears

‘End of NHS’ if chancellor doesn’t reverse mini-budget

He argued his fiscal strategy was focused on the medium-term, and was aimed at showing voters “we can be more efficient in how we spend taxpayers’ money”.

He went on to say that the economic situation would be better in 2024, before what he said was always going to be a “tricky” general election – with Labour currently surging ahead in the polls.

He told MPs that he was establishing a “good working relationship” with the governor of the Bank of England and was in daily contact with him.

He also acknowledged that markets had been volatile but said they were now “settling down” and argued the turmoil reflected a frustration that the markets had not known everything that was included in the mini-budget.

The taxpayer is to help drive the switch to non-polluting vehicles through a new grant of up to £3,750, but some of the cheapest electric cars are to be excluded.

The Department for Transport (DfT) said a £650m fund was being made available for the Electric Car Grant, which is due to get into gear from Wednesday.

Users of the scheme – the first of its kind since the last Conservative government scrapped grants for new electric vehicles three years ago – will be able to secure discounts based on the “sustainability” of the car.

Money latest: easyJet bereavement policy faces refund question

It will apply only to vehicles with a list price of £37,000 or below – with only the greenest models eligible for the highest grant.

Buyers of so-called ‘Band two’ vehicles can receive up to £1,500.

The qualification criteria includes a recognition of a vehicle’s carbon footprint from manufacture to showroom so UK-produced EVs, costing less than £37,000, would be expected to qualify for the top grant.

It is understood that Chinese-produced EVs – often the cheapest in the market – would not.

BYD electric vehicles before being loaded onto a ship in Lianyungang, China. Pic: Reuters

DfT said 33 new electric car models were currently available for less than £30,000.

The government has been encouraged to act as sales of new electric vehicles are struggling to keep pace with what is needed to meet emissions targets.

Challenges include the high prices for electric cars when compared to conventionally powered models.

At the same time, consumer and business budgets have been squeezed since the 2022 cost of living crisis – and households and businesses are continuing to feel the pinch to this day.

Another key concern is the state of the public charging network.

The Chinese electric car rivalling Tesla

Transport Secretary Heidi Alexander said: “This EV grant will not only allow people to keep more of their hard-earned money – it’ll help our automotive sector seize one of the biggest opportunities of the 21st century.

“And with over 82,000 public charge points now available across the UK, we’ve built the infrastructure families need to make the switch with confidence.”

The Government has pledged to ban the sale of new fully petrol or diesel cars and vans from 2030 but has allowed non-plug in hybrid sales to continue until 2025.

It is hoped the grants will enable the industry to meet and even exceed the current zero emission vehicle mandate.

Under the rules, at least 28% of new cars sold by each manufacturer in the UK this year must be zero emission.

The figure stood at 21.6% during the first half of the year.

The car industry has long complained that it has had to foot a multi-billion pound bill to woo buyers for electric cars through “unsustainable” discounting.

Mike Hawes, chief executive of the Society of Motor Manufacturers and Traders, said the grants sent a “clear signal to consumers that now is the time to switch”.

He went on: “Rapid deployment and availability of this grant over the next few years will help provide the momentum that is essential to take the EV market from just one in four today, to four in five by the end of the decade.”

But the Conservatives questioned whether taxpayers should be footing the bill.

Shadow transport secretary Gareth Bacon said: “Last week, the Office for Budget Responsibility made clear the transition to EVs comes at a cost, and this scheme only adds to it.

“Make no mistake: more tax rises are coming in the autumn.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike