UK economy finds reverse gear with surprise decline in October

The UK economy took a surprise tumble in October, according to an early official estimate that showed a contraction of 0.3%.

The Office for National Statistics (ONS) reported that output in all three main divisions – services, manufacturing and construction – was in negative territory.

Economists had expected a flat performance, following on from the 0.2% growth seen in September.

That meagre figure helped the economy to zero growth for the third quarter of the year, easing concerns over the prospect for a recession which is realised if a country records two consecutive quarters of contraction.

Nevertheless, the latest data builds on expectations of a largely flat performance ahead, despite a series of growth measures announced by the chancellor in his autumn statement last month.

Jeremy Hunt said of the ONS figures: “It is inevitable GDP (gross domestic product) will be subdued whilst interest rates are doing their job to bring down inflation.”

Action taken by the Bank of England since December 2021 to tame inflation was intended to hit demand in the economy, helping the pace of price growth ease.

While the rate of inflation has slowed considerably from the figure above 11% seen just over a year ago, prices are still rising but just at a steadier pace.

The effect of interest rate hikes imposed by the Bank has added to borrowing costs, with rising mortgage and rent bills becoming a key plank of the cost of living crisis.

How bad is the UK’s economy?

The Bank warned earlier this month that five million households were yet to feel the home loan hit because their fixed terms had not expired.

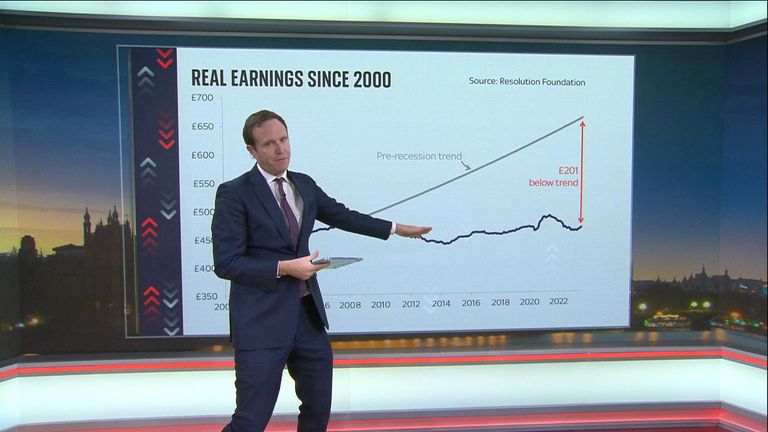

Household spending power has, to some extent, been propped up by a record pace for wage growth but data on Tuesday showed sharp falls in the levels of awards.

Consumers were still, however, enjoying the best real wage growth – when inflation is accounted for – for two years due to the steep easing in the inflation rate in October.

The Bank’s monetary policy committee has seen enough progress in bringing inflation down to have kept Bank rate at 5.25% for two consecutive meetings.

It is due to outline its next rate decision on Thursday, with financial markets and economists widely expecting a further pause.

ONS director of economic statistics, Darren Morgan, said of Wednesday’s data: “Our initial estimates suggest that GDP growth was flat across the last three months.

“Increases in services, led by engineering, film production and education – which recovered from the impact of summer strikes – were offset by falls in both manufacturing and housebuilding.

“October, however, saw contractions across all three main sectors. Services were the biggest driver of the fall with drops in IT, legal firms and film production – which fell back after a couple of strong months.

“These were also compounded by widespread falls in manufacturing and construction, which fell partly due to the poor weather.”

Shadow chancellor Rachel Reeves said: “Rishi Sunak ends the year having failed to deliver on his own promise to grow the economy.

“Economic growth is going backwards leaving working people worse off,” she said.

Business

Post Office Capture scandal: Sir Alan Bates calls for those responsible for wrongful convictions to be ‘brought to account’

Sir Alan Bates has called for those responsible for the wrongful convictions of sub postmasters in the Capture IT scandal to be “brought to account”.

It comes after Sky News unearthed a report showing Post Office lawyers knew of faults in the software nearly three decades ago.

The documents, found in a garage by a retired computer expert, describe the Capture system as “an accident waiting to happen”.

Post Office: The lost ‘Capture’ files

Sir Alan said the Sky News investigation showed “yet another failure of government oversight; another failure of the Post Office board to ensure [the] Post Office recruited senior people competent of bringing in IT systems” and management that was “out of touch with what was going on within its organisation”.

The unearthed Capture report was commissioned by the defence team for sub postmistress Patricia Owen and served on the Post Office in 1998 at her trial.

It described the software as “quite capable of producing absurd gibberish” and concluded “reasonable doubt” existed as to “whether any criminal offence” had taken place.

Ms Owen was found guilty of stealing from her branch and given a suspended prison sentence.

She died in 2003 and her family had always believed the computer expert, who was due to give evidence on the report, “never turned up”.

Patricia Owen (right) was convicted in 1998 of stealing from her post office branch. She died in 2003

Adrian Montagu reached out after seeing a Sky News report earlier this year and said he was actually stood down by the defending barrister with “no reason given”.

The barrister said he had no recollection of the case.

Victims and their lawyers hope the newly found “damning” expert report, which may never have been seen by a jury, could help overturn Capture convictions.

Read more: Post Office scandal redress must not only be fair – it must be fast

What is the Capture scandal?

‘These people have to be brought to account’

Sir Alan, the leading campaigner for victims of the Horizon Post Office scandal, said while “no programme is bug free, why [was the] Post Office allowed to transfer the financial risk from these bugs on to a third party ie the sub postmaster, and why did its lawyers continue with prosecutions seemingly knowing of these system bugs?”

He continued: “Whether it was incompetence or corporate malice, these people have to be brought to account for their actions, be it for Capture or Horizon.”

More than 100 victims have come forward

More than 100 victims, including those who were not convicted but who were affected by the faulty software, have so far come forward.

Capture was used in 2,500 branches between 1992 and 1999, just before Horizon was introduced – which saw hundreds wrongfully convicted.

The Criminal Cases Review Commission (CCRC), the body responsible for investigating potential miscarriages of justice, is currently looking at a number of Capture convictions.

A CCRC spokesperson told Sky News: “We have received applications regarding 29 convictions which pre-date Horizon.

25 of these applications are being actively investigated by case review managers, and two more recent applications are in the preparatory stage and will be assigned to case review managers before the end of June.

“We have issued notices under s.17 of the Criminal Appeal Act 1995 to Post Office Ltd requiring them to produce all material relating to the applications received.

“To date, POL have provided some material in relation to 17 of the cases and confirmed that they hold no material in relation to another 5. The CCRC is awaiting a response from POL in relation to 6 cases.”

A spokesperson for the Department for Business and Trade said: “Postmasters negatively affected by Capture endured immeasurable suffering. We continue to listen to those who have been sharing their stories on the Capture system, and have taken their thoughts on board when designing the Capture Redress Scheme.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike