Woolworths demise 15 years on: What happened at the retail giant and could it come back?

Parachuted in to turn around a failing giant of the British high street, Robert McDonald was part of Woolworths’s last roll of the dice.

The new finance director said he was excited to join an “iconic” brand when he began work in early November 2008, but just three weeks later the company would sink into administration.

And there was little the company’s last ever executive hire could do to stop the famous store – known for its pick ‘n’ mix, homeware and everything in between – from closing for good on 6 January 2009.

“Like everyone my age, I had grown up thinking its existence was a normal part of life,” Mr McDonald told Sky News.

“I was very pleased to have the opportunity to work there. I knew it was going through hard times and looked forward to being able to help.

“But, sadly, it was past that by the time I joined, and the end seemed very swift.”

Analysts blame its downfall on a toxic combination of low cash reserves, lost credit insurance and crippling debt – all exacerbated by the 2008 financial crisis.

It marked the end of Woolies’s near century-long presence on the high street, with more than 800 stores closed down and about 27,000 jobs lost.

Woolworths was popular for its pic ‘n’ mix

For many of its staff, news of Woolworths’s demise into administration came from the media, with earlier rumours confirmed in reports on 26 November 2008.

Paul Seaton, who had worked as a store manager and as part of the IT team during 25 years at the company, said his colleagues “crowded around the TV” to hear their worst fears confirmed.

“It just all fell to pieces after that,” Mr Seaton, now 61, told Sky News.

“The sad reality is Woolworths took 99 years to build, and it took 42 days from administration to the day the last door shut. 99 years of meticulous care and thought… gone.”

The board insisted administration wouldn’t detract from “business as usual”, Mr Seaton said, but that all changed when he was called to a meeting on 5 December.

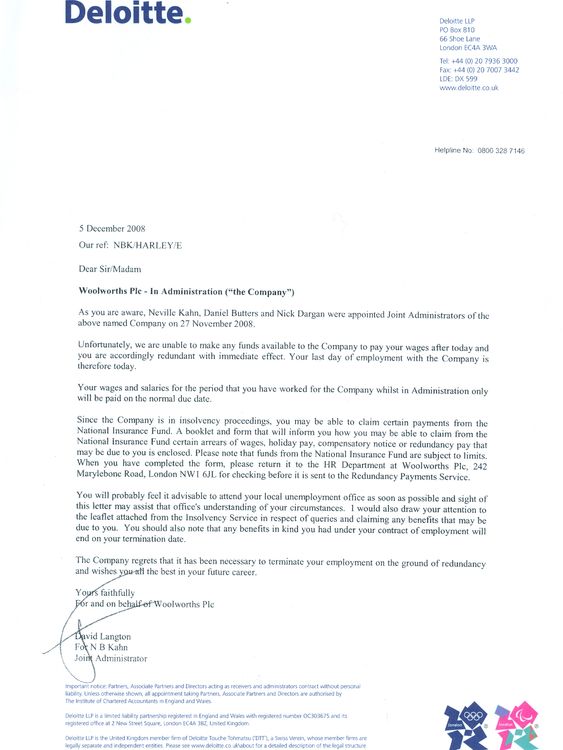

He was among 500 senior figures gathered at Woolworths HQ, where each was given a letter written by administrators Deloitte notifying none would be paid another day and all had lost their jobs with immediate effect.

The notice given by Deloitte to Paul Seaton

“We were summoned and told not to come back, all 500 of us,” Mr Seaton said, adding their passes into the building were deactivated on the spot. “The business only carried on for one month after that.”

While his time at the company came to an abrupt end, he dedicated time to creating a virtual Woolworths museum, preserving memorabilia and documenting the chain’s long history.

A store for the family

The first store opened in November 1909 in Liverpool, by New Yorker Frank Woolworth, who had already established the brand in the US.

In a prescient diary entry, he wrote during an earlier trip to Europe that “a good penny and sixpence store, run by a live Yankee, would be a sensation here”.

Such was the success of the UK counterpart, his successor Byron Miller reportedly beamed that “the child has long since outgrown the parent”.

Mr Seaton thinks the literal child-parent relationship was key to the store’s popularity.

“There used to be old adage that people need Tesco because everyone has to eat, and people trust Boots because you call the manager ‘doctor’, but they went to Woolworths because they love Woolworths,” he said.

“Have you ever heard a kid saying ‘mum I want to go to Tesco’? The whole reason I loved being a manager is kids and families loved coming to Woolworths.”

Paul Seaton with Woolworths memorabilia collected over the years

The store’s name lives on in Australia – though has no connection with US or UK equivalents – where it is the country’s largest supermarket chain and last year recorded a net profit of $1.62bn (about £87bn).

US stores closed in 1997, but the UK branches recorded a record profit topping £100m just one year later.

What went wrong?

Customers were still shopping at the UK stores, and in the firm’s final annual report the company made a slight pre-tax profit in 2007.

But even with some signs of recovery ahead of 2008, Woolworths had a terminal problem: modest cash flow and a £385m mountain of debt.

Retail expert Clare Bailey was among the consultants drafted in 2006 to tackle the mammoth task of detangling the company’s supply chain, which she says was collecting too much of some stock and too little of others.

As banks began to lose faith in Woolworths’s finances, the firm had its credit insurance withdrawn – meaning it had to pay suppliers immediately, rather than in instalments.

To make matters worse, many Woolworths stores were sold a few years before and rented back at a price that only appeared to increase over the years.

Left with fewer assets, little in way of cash reserves and no credit insurance, the retailer was not prepared for the coming shock of the 2008 financial crisis.

“Cashflow is like oxygen,” Ms Bailey told Sky News. “You can be profitable, but if you haven’t got cash to pay bills or for when something goes wrong, then that’s it – game over.”

The company reported a pre-tax loss of £90.8m over the first half of 2008 in September that year, despite launching the WorthIt range – promoting low-cost products – in 2007.

Losing sales and customers

One of the big issues Ms Bailey identified in the supply chain was a failure to keep evergreen products on shelves.

For example, she said only 20 stores out of more than 800 nationwide had the correct amount of coat hangers, a product that sells all year, while others bought far too many Christmas trees.

It meant money was “trapped in stocks”, she said, and would gradually turn customers away.

“And if you replicate that through other products, customers could find what they didn’t want, but not what they wanted,” she said.

“You might, as a customer, give them the benefit of the doubt a few times, but eventually they will turn to other places. So, they not only lost the sale – they also lost the customers.”

It’s this perceived neglect of the customer journey that small business growth expert Claire Hancott believes cost Woolworths at the turn of the century.

Footfall almost halved from 7.5 million in 2000 to around 4.5 million in 2007, she said, while the market for Woolworths’s once-popular CDs was shrinking as more consumers headed to the internet.

“Businesses can’t ignore these big trends, even if they won’t come into play for years,” Ms Hancott told Sky News.

“Blockbusters was a classic example, when they thought digital films wouldn’t take off.

“Woolworths wasn’t at the forefront of consumer technology and it’s so important to be looking 10, 20 years into the future – it takes a long time to prepare.”

Discount stores such as pound shops began to pop up on the high street, adding to growing competition that ultimately forced an attempt to sell the company in November 2008 for – ironically – just £1.

It was hoped a sale to restructuring experts Hilco would give them the job of repaying the debt, but the banks rejected the move.

The company went into administration just days later.

A false dawn, but will the sun rise on Woolworths again?

Ever since the company collapsed under the weight of its debt, rumours of a potential return to the high street have never been completely quashed.

A fake announcement – made by a social media account falsely claiming to be run by Woolworths – heralding a comeback was met with excitement in 2020, with savings platform Raisin UK reporting 44% of people discussing the store’s revival online “loved the news”.

The post turned out to be false

In August 2022, pollsters at YouGov found 49% of survey respondents said they wished they could bring back Woolies – a far higher proportion than any other defunct chain.

But for all the hopes of an encore, some of those involved with the firm rue the time that has since been lost – and believe it may have even survived.

“I came in at the end of 2006, but the work we were doing can take three or five years,” Ms Bailey said. “Maybe they started too late.”

All but a small handful of the Woolworths stores were re-let to other retailers within a decade, she added, meaning the spaces “still had merit in the local community”.

“The inner workings of a business are quite complicated,” she said.

“But I think it’s a sad situation it collapsed, because – had they been given a stay of execution – they may well have been successful in turning it around.”

Read more:

Christmas tree from 1920s Woolworths sells for ‘astonishing’ price

Next raises profit forecast but warns stock could be delayed by Red Sea attacks

Ms Hancott agrees: “In another time, would it have crumbled? That’s the million-pound question that nobody will be able to answer.

“Had it not been in the midst of a crisis, then it may have survived.”

For Mr McDonald, a chance to draw on his experience handling company finances never materialised.

It was, nonetheless, a “fascinating experience”, he said.

“It’s such a shame we didn’t have longer to turn that business around,” he said.

“I joined as part of a turnaround plan, but it was too late to change the course of history.”

Nadhim Zahawi, the former chancellor, is to be named as chairman of one of Britain’s biggest online retailers, days after confirming that he would step down from parliament at the next general election.

Sky News has learnt that Mr Zahawi is to be appointed non-executive chair of Very Group, the largest remaining part of the Barclay family’s business empire.

Sources said the appointment, which will see him replacing interim chair Aidan Barclay, would be announced on Monday.

His arrival at Very Group will come during a period of turbulence for the Barclay family, who own The Daily Telegraph but are unable to exert influence over it under a government order while its future ownership remains uncertain, subject to a forthcoming auction.

Mr Zahawi’s appointment at Very Group, first revealed by Sky News in March, is likely to prompt a search for fresh equity investment in the near term, as well as a broader review of its capital structure.

The company, which owns the Very and Littlewoods brands, is weighed down by debt, but has nearly 4.5 million customers and significant expansion targets.

Based in Liverpool, it sells electrical goods, homewares and fashion, backed by a large consumer finance arm.

It is said to have performed resiliently despite uncertainty over its ownership.

The company recently said it had secured £125m of new debt funding from Carlyle Global Credit and IMI, which the company has said is designed to support future growth.

Mr Zahawi, the MP for Stratford-on-Avon since 2010, had a brief stint as chancellor of the exchequer, while he also held ministerial posts at the Department of Health and Social Care – where he oversaw the vaccine rollout during the COVID pandemic – the Department for Business and as chancellor of the Duchy of Lancaster.

He was made Conservative Party chairman by Rishi Sunak but was dismissed for failing to disclose he was being investigated by HMRC and the National Crime Agency over a multi-million pound tax dispute related to the sale of shares in his polling firm YouGov while he was chancellor.

He said he had made a “careless and not deliberate” error after initially saying he had no knowledge of the investigation and had “paid all taxes”.

February 2023 – Zahawi: Starmer grills Sunak

Mr Zahawi’s announcement last week that he would not stand again at the next election meant he joined the likes of Theresa May, the ex-prime minister, and former Conservative Party chairman Sir Brandon Lewis in deciding to leave parliament.

Prior to his political career, he was the founder of YouGov, while he is now a patron of the Adam Smith Institute, the economic thinktank.

Read more from Sky News:

Seven companies granted royal warrants from Queen

Wales becomes first UK nation to join metaverse

Mr Zahawi has been playing a role as an intermediary between the Barclay family and the Abu Dhabi-based investor IMI Investments since its interest in participating in a bid for The Daily Telegraph emerged last summer.

He had been tipped to chair the newspaper group if RedBird IMI, a vehicle fronted by former CNN president Jeff Zucker, had been successful in buying it.

However, a fierce backlash from Conservative parliamentarians prompted Downing Street to intervene and amend legislation to prohibit ownership of British newspaper titles by investors connected to a foreign state.

RedBird IMI is now finalising preparations to conduct a further auction of the Telegraph newspapers and The Spectator magazine.

The Barclays, who used to own London’s Ritz hotel, have already lost control of several of their corporate assets.

In February, Yodel Group, their parcel delivery business, narrowly averted insolvency when it was sold to a consortium backed by executives at Shift, a rival.

The parent company of ArrowXL, another delivery firm they own, had been forced into administration by HSBC, its principal lender.

Half of the £1.2bn loan that the Barclays took from RedBird IMI and IMI was secured against their media assets, with the bulk of the remainder said to have been secured against other assets including Very Group.

At various points in the last decade, the Telegraph proprietors have explored a sale of the online shopping business, having valued it at over £3bn.

Very Group and Mr Zahawi both declined to comment.

The major backer of Pinewood Studios is among the suitors vying to buy Village Hotels, one of Britain’s biggest mid-market hotel chains.

Sky News understands Aermont, which specialises in real estate-backed investments, submitted an offer last week for Village Hotels, which is owned by KSL Capital Partners.

City sources said KSL was seeking offers worth in the region of £850m or more.

A number of other parties are also understood to have tabled bids ahead of a deadline last week.

Blackstone, the giant private equity firm, is considering making an offer but has yet to do so, according to insiders.

The auction is being handled by bankers at Morgan Stanley.

It comes months after attempts to sell Center Parcs UK were called off, while a mooted sale of Travelodge has so far failed to result in a deal.

Village Hotels comprises a portfolio of more than 30 properties from Aberdeen to Bournemouth, with rooms available at budget prices.

Founded in 1995 as Village Urban Resorts, the hotels feature pub-style restaurants and gyms.

KSL was reported to have paid £485m for the business when it bought it in 2014 from De Vere Group.

Keep up with all the latest news from the UK and around the world by following Sky News

Read more:

Motors.co.uk among suitors raiding stricken Cazoo’s garage sale

Former IPO candidate Fruugo hires bankers to explore sale

The Denver, Colorado-based buyout firm has also owned other UK hotel chains including Hotel du Vin and Malmaison.

Aermont and Blackstone declined to comment.

Henry Birch, the former boss of Rank Group, is among the candidates vying to run Entain, the FTSE-100 owner of Ladbrokes.

Sky News has learnt that Mr Birch is one of a small number of candidates being considered by Entain to replace Jette Nygaard-Andersen as its permanent chief executive.

The recruitment process comes at a challenging time for Entain, which has been beset by boardroom upheaval and regulatory difficulties in various international markets.

Its stock has halved in the last year, leaving it with a market capitalisation of just under £5bn.

This weekend, sources close to the company confirmed that Mr Birch was a serious contender for the post, although they said others were also in contention.

An appointment could still be weeks or even a small number of months away, they added.

Henry Birch, former CEO of Very Group

Mr Birch stepped down as chief executive of Very Group, the online retailer owned by the Barclay family, in 2022.

He is an experienced gambling industry executive, having spent four years as chief executive of William Hill Online prior to joining the London-listed multichannel gaming operator Rank Group.

He has also held roles at Leisure & Gaming plc and BettingCorp.

Under Mr Birch, Very Group broke the £2bn annual sales mark for the first time.

Investors in Entain have been pressing its board to recruit a new chief executive with substantial gambling experience as it grapples with a plunging share price and numerous regulatory and strategic challenges.

Last week, Sky News revealed that former bosses of bookies Coral and Skybet had rejected overtures to become its new boss.

Pic: Reuters

Industry sources said that Dan Taylor, chief executive of Flutter Entertainment’s international operations, had also been approached, although it was unclear whether he was interested.

Entain has been under siege from activist investors for months.

In January, it announced that Ricky Sandler, who runs Entain shareholder Eminence Capital, would join its board as a non-executive director.

Last month, it said that Barry Gibson, its chairman, would retire later this year and be replaced by interim chair, and former acting CEO, Stella David.

Entain has hired bankers to sell PartyPoker and other non-core operations, which the Financial Times reported could include Netherlands-based BetCity, which Entain bought for £398mn last year.

As well as Ladbrokes, Entain owns Coral and a stake in BetMGM, a major US betting player.

Read more on Sky News:

Calls for arena ticket levy and tax relief

British Airways owner’s profits soar

Interest rate held for sixth consecutive time

Keep up with all the latest news from the UK and around the world by following Sky News

MGM Resorts, the US casino operator behind the Bellagio in Las Vegas, attempted to buy Entain in 2021 but was rebuffed at a much higher valuation than the UK company’s shares trade at now.

MGM has since ruled out a further bid, although analysts expect it to return at some stage.

The company has faced a deluge of regulatory problems, triggering sharp criticism of its governance and business practices.

Last December, it was ordered to pay £615m for failing to prevent bribery at its former Turkish subsidiary under a deferred prosecution agreement.

Shares in Entain closed at 778.8p on Friday, giving the company a market capitalisation of £4.98bn.

Entain declined to comment, while Mr Birch could not be reached for comment.

-

Sports2 years ago

Sports2 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Environment12 months ago

Environment12 months agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports1 month ago

Sports1 month agoStory injured on diving stop, exits Red Sox game

-

Sports7 months ago

Sports7 months agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment1 year ago

Environment1 year agoGame-changing Lectric XPedition launched as affordable electric cargo bike

-

Environment1 year ago

Environment1 year agoTesla advances Powerwall pilot project with German electric company