UnitedHealth Group has paid more than $3 billion to providers following cyberattack

In this photo illustration the UnitedHealth Group logo displayed on a smartphone screen.

Sheldon Cooper | Sopa Images | Lightrocket | Getty Images

UnitedHealth Group has paid out an additional $1 billion to providers that have been impacted by the Change Healthcare cyberattack since last week, bringing the total amount of funds advanced to more than $3.3 billion, the company said on Wednesday.

UnitedHealth, which owns Change Healthcare, discovered in February that a cyber threat actor had breached part of the unit’s information technology network. Change Healthcare processes more than 15 billion billing transactions annually, and one in every three patient records passes through its systems, according to its website.

The company disconnected the affected systems “immediately upon detection” of the threat, according to a filing with the SEC. The interruptions left many health-care providers temporarily unable to fill prescriptions or get reimbursed for their services by insurers.

Many health-care providers rely on reimbursement cash flow to operate, so the fallout has been substantial. Smaller and mid-sized practices told CNBC they were making tough decisions about how to stay afloat. A survey published by the American Hospital Association earlier this month found that 94% of hospitals have experienced financial disruptions from the attack.

As a result, UnitedHealth introduced its temporary funding assistance program to help providers in need of support. The company said the $3.3 billion in advances will not need to be repaid until claims flows return to normal. Federal agencies like the Centers for Medicare & Medicaid Services have introduced additional options to ensure that states and other stakeholders can make interim payments to providers, according to a release.

UnitedHealth has been working to restore Change Healthcare’s systems in recent weeks, and it expects some disruptions will continue into April, according to its website. The company began processing a backlog of more than $14 billion in claims on Friday, and on Wednesday said, “claims have begun to flow.”

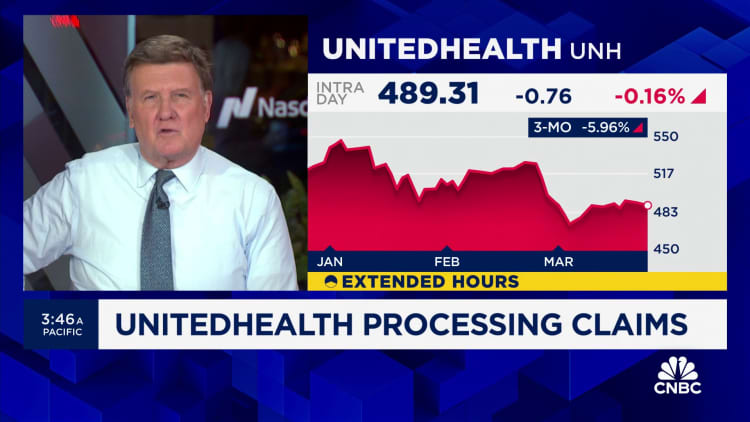

Shares of UnitedHealth have fallen more than 6% since the attack was disclosed.

Late last month, the company said the ransomware group Blackcat is behind the attack. Blackcat, also called Noberus and ALPHV, steals sensitive data from institutions and threatens to publish it unless a ransom is paid, according to a December release from the U.S. Department of Justice.

The Department of State on Wednesday announced it’s offering a reward of up to $10 million for information that could help identify or locate cyber actors linked to Blackcat.

UnitedHealth said Wednesday that it’s “still determining the content of the data that was taken by the threat actor.” The company said a “leading vendor” is analyzing the impacted data. United Health is working closely with law enforcement and third parties like Palo Alto Networks and Google‘s Mandiant to assess the attack.

“We continue to be vigilant, and to date have not seen evidence of any data having been published on the web,” UnitedHealth said. “And we are committed to providing appropriate support to people whose data is found to have been compromised.”

Rep. Jamie Raskin, D-Md., ranking member of the House Committee on Oversight and Accountability, wrote a letter to UnitedHealth CEO Andrew Witty on Monday requesting information about the “scope and extent” of the breach.

Raskin asked Witty for information about when Change Healthcare notified its clients about the breach, what specific infrastructure and information was targeted and what cybersecurity procedures the company has in place. The committee requested written responses “no later” than April 8.

“Given your company’s dominant position in the nation’s health care and health insurance industry, Change Healthcare’s prolonged outage as a result of the cyberattack has already had ‘significant and far-reaching’ consequences,” Raskin wrote.

The Biden administration also launched an investigation into UnitedHealth earlier this month due to the “unprecedented magnitude of the cyberattack,” according to a statement.

WATCH: UnitedHealth unit begins processing $14 billion medical claims backlog

Chief executive officer of Google Sundar Pichai.

Marek Antoni Iwanczuk | Sopa Images | Lightrocket | Getty Images

Google on Friday made the latest a splash in the AI talent wars, announcing an agreement to bring in Varun Mohan, co-founder and CEO of artificial intelligence coding startup Windsurf.

As part of the deal, Google will also hire other senior Windsurf research and development employees. Google is not investing in Windsurf, but the search giant will take a nonexclusive license to certain Windsurf technology, according to a person familiar with the matter. Windsurf remains free to license its technology to others.

“We’re excited to welcome some top AI coding talent from Windsurf’s team to Google DeepMind to advance our work in agentic coding,” a Google spokesperson wrote in an email. “We’re excited to continue bringing the benefits of Gemini to software developers everywhere.”

The deal between Google and Windsurf comes after the AI coding startup had been in talks with OpenAI for a $3 billion acquisition deal, CNBC reported in April. OpenAI did not immediately respond to a request for comment.

The move ratchets up the talent war in AI particularly among prominent companies. Meta has made lucrative job offers to several employees at OpenAI in recent weeks. Most notably, the Facebook parent added Scale AI founder Alexandr Wang to lead its AI strategy as part of a $14.3 billion investment into his startup.

Douglas Chen, another Windsurf co-founder, will be among those joining Google in the deal, Jeff Wang, the startup’s new interim CEO and its head of business for the past two years, wrote in a post on X.

“Most of Windsurf’s world-class team will continue to build the Windsurf product with the goal of maximizing its impact in the enterprise,” Wang wrote.

Windsurf has become more popular this year as an option for so-called vibe coding, which is the process of using new age AI tools to write code. Developers and non-developers have embraced the concept, leading to more revenue for Windsurf and competitors, such as Cursor, which OpenAI also looked at buying. All the interest has led investors to assign higher valuations to the startups.

This isn’t the first time Google has hired select people out of a startup. It did the same with Character.AI last summer. Amazon and Microsoft have also absorbed AI talent in this fashion, with the Adept and Inflection deals, respectively.

Microsoft is pushing an agent mode in its Visual Studio Code editor for vibe coding. In April, Microsoft CEO Satya Nadella said AI is composing as much of 30% of his company’s code.

The Verge reported the Google-Windsurf deal earlier on Friday.

Technology

Nvidia’s Jensen Huang sells more than $36 million in stock, catches Warren Buffett in net worth

Jensen Huang, CEO of Nvidia, holds a motherboard as he speaks during the Viva Technology conference dedicated to innovation and startups at Porte de Versailles exhibition center in Paris, France, on June 11, 2025.

Gonzalo Fuentes | Reuters

Nvidia CEO Jensen Huang unloaded roughly $36.4 million worth of stock in the leading artificial intelligence chipmaker, according to a U.S. Securities and Exchange Commission filing.

The sale, which totals 225,000 shares, comes as part of Huang’s previously adopted plan in March to unload up to 6 million shares of Nvidia through the end of the year. He sold his first batch of stock from the agreement in June, equaling about $15 million.

Last year, the tech executive sold about $700 million worth of shares as part of a prearranged plan. Nvidia stock climbed about 1% Friday.

Huang’s net worth has skyrocketed as investors bet on Nvidia’s AI dominance and graphics processing units powering large language models.

The 62-year-old’s wealth has grown by more than a quarter, or about $29 billion, since the start of 2025 alone, based on Bloomberg’s Billionaires Index. His net worth last stood at $143 billion in the index, putting him neck-and-neck with Berkshire Hathaway‘s Warren Buffett at $144 billion.

Shortly after the market opened Friday, Fortune‘s analysis of net worth had Huang ahead of Buffett, with the Nvidia CEO at $143.7 billion and the Oracle of Omaha at $142.1 billion.

The company has also achieved its own notable milestones this year, as it prospers off the AI boom.

On Wednesday, the Santa Clara, California-based chipmaker became the first company to top a $4 trillion market capitalization, beating out both Microsoft and Apple. The chipmaker closed above that milestone Thursday as CNBC reported that the technology titan met with President Donald Trump.

Brooke Seawell, venture partner at New Enterprise Associates, sold about $24 million worth of Nvidia shares, according to an SEC filing. Seawell has been on the company’s board since 1997, according to the company.

Huang still holds more than 858 million shares of Nvidia, both directly and indirectly, in different partnerships and trusts.

WATCH: Nvidia hits $4 trillion in market cap milestone despite curbs on chip exports

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike