Shared ownership: ‘We can’t afford it. It makes a mockery of being in social housing’

Josie Dom, 53, was thrilled when she moved into her new home in October.

She bought 30% of it through the shared ownership scheme as an affordable route to home ownership, even if it was only partial ownership.

The idea is to help people who would not be able to buy a home outright get on to the housing ladder earlier by buying a share of a property and paying subsidised rent on the rest – often to a non-profit housing association.

Without it, she says there was no way for her and her two children to stay in Colchester, where they love living and attend school and college.

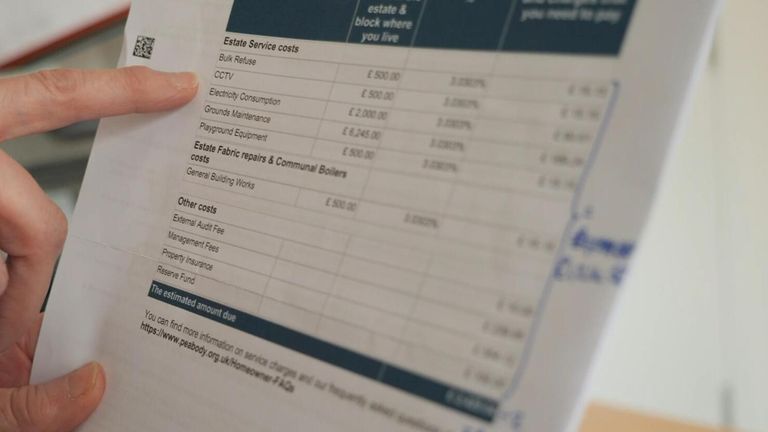

But her enthusiasm started waning when after just six months, the housing association increased the building’s service charges by 138%, from £85 to £202 per month.

While she had anticipated small annual rises, this unexpectedly large jump was unaffordable.

“Obviously the idea of shared ownership is to help people like me that wouldn’t otherwise be able to afford their own home,” said Ms Dom.

“Then suddenly, again, we can’t afford it. It makes a mockery of being shared ownership and having social housing.”

Josie Dom tells Sky News about her service charge increases at her new shared ownership home

The expanded scheme now makes up half of affordable homes funding.

Sky News has been approached by dozens of other shared owners facing soaring costs and other issues, including difficulty selling.

With rising mortgage costs this relatively cheaper option appears to be increasingly appealing to buyers.

Rightmove, the UK’s largest online property website, told Sky News shared ownership properties are taking 56 days to sell versus 65 days for all other properties on average, as of March 2024.

And interest has increased over time – they said demand is up 37% from a year ago for shared ownership properties.

Initially low costs can be misleading, however.

Barry Gardiner, Labour MP for Brent, was on the government’s shared ownership cross parliamentary report committee.

He told Sky News: “They don’t actually have the rights of control that full ownership ought to give because you are both a tenant and a share in the ownership – and you’re paying the full service charge on the property.

“People just find it a desperate trap.”

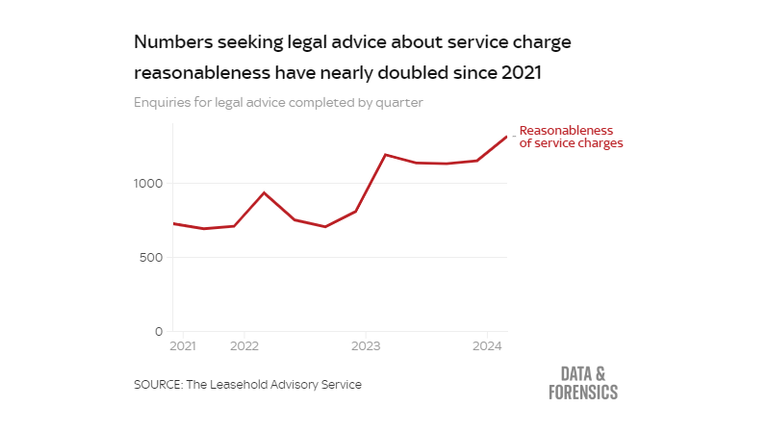

Record numbers are seeking legal advice

Data from The Leasehold Advisory Service (LEASE) shows the number of leaseholders seeking legal advice about service charges has increased in recent years.

The number of enquiries dealt with about the reasonableness of service charges has nearly doubled compared with 2021.

There were over 1,300 enquiries in the three months to March 2024, the highest number since records beginning in 2018.

LEASE joint CEOs Sally Frazer and Alice Bradley told Sky News they are concerned about the increase, “particularly over the last year”.

“More broadly we know there is still not enough awareness of the service and support our organisation can offer,” they added.

Feeling trapped

Affordability and freedom are typical selling points advertised to buyers, as well as the opportunity to “staircase” towards higher ownership shares while saving money on rent.

But for Alex, who bought 25% of his north London flat in 2019, the very opposite has been true. The dream of home ownership has become a nightmare, leaving him and many others in his building feeling trapped.

In February, residents were told by their property management company James Andrew Residential (JAR) that the service charge would be more than tripling, from £500 to £1,700 per month from April.

His rent and service charge are now over £2,900 per month, and the mortgage is an additional £800.

Fitzgerald Court, where service charges have increased from £500 to £1,700 per month

“My partner and I just got engaged, but we can’t plan the wedding. All our money is going to keeping us in the flat, and now we’re using up our existing savings,” he told Sky News.

“In 2019 it seemed like a great affordable option, but now we would be better off if we were renting and are worried about being able to sell at all.”

In response to residents’ concerns, the property managers JAR told Sky News they were engaging with owners and investigating the matter to see if costs can be mitigated.

Islington and Shoreditch Housing Association, who own the other share of Alex’s flat, told Sky News the service charge increase is “outrageous and not justifiable”.

They said: “We firmly disagree with JAR’s assessment that the residents should bear such major maintenance costs for a six-year-old building”.

“We will be challenging the cost increase on behalf of our residents and will go to tribunal to fight it if we must.”

Leasehold reform is needed

The issue of leasehold charges is not unique to shared owners and has been recognised as a wider industry issue.

“The problem lies in the leasehold structure of the housing market and its application to shared ownership,” said Stanimara Milcheva, Professor in Real Estate Finance at University College London.

Service charges are often dictated by the management company which may also own the freehold.

Prof Milcheva added there should be more transparency, so shared ownership buyers have more access to relevant information about service charges in their region.

Stanimara Milcheva, Professor in Real Estate Finance at University College London

The government introduced the Renters Reform Bill to parliament in 2023, a piece of legislation that aims to improve conditions for renters, but which has wider implications for the leasehold sector.

Its proposed measures to regulate service charges include greater transparency and breakdowns of costs, and the exclusion of insurance costs. But it is unclear when, or if, the currently delayed Bill will make it through Parliament in its present form.

These issues do have the potential to cause more financial stress to shared owners, who are typically earning lower incomes than those who buy their first home outright.

From preliminary research, Prof Milcheva and colleagues found that the gross income of the main first-time shared ownership buyer was on average 23% lower, at £42k compared to £55k for those buying outright, between 2015 and 2023.

The most affected region is London

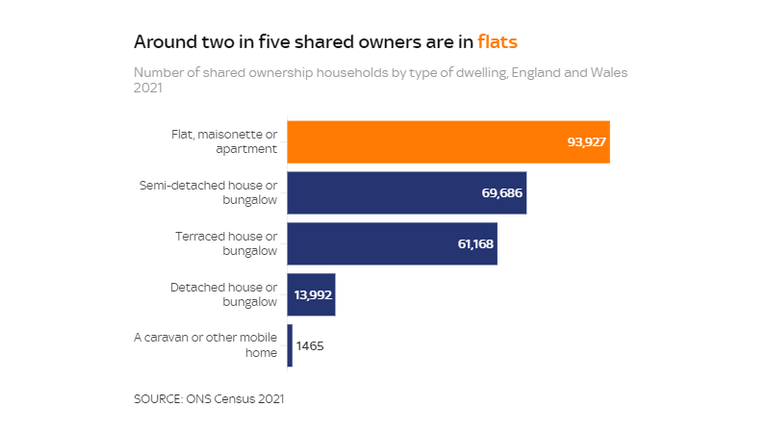

Service charges do not affect all shared owners, as although most are leaseholders the majority live in houses.

Still, close to 94,000 (40%) of shared ownership households are in flats, based on the latest estimates from the 2021 Census.

Nearly half of these (43,000 households) are in London, while outside of London the proportion of those in flats falls to 27%.

“Service charges are more of a problem in London, where pretty much the entire stock of shared ownership are apartments,” said Prof Milcheva.

This has an impact on the relative costs of service charges, which are as much as triple the price in London relative to rent costs, at 30% of rent compared to 10%-13% in other areas, according to their research.

Shared ownership has now overtaken social rent

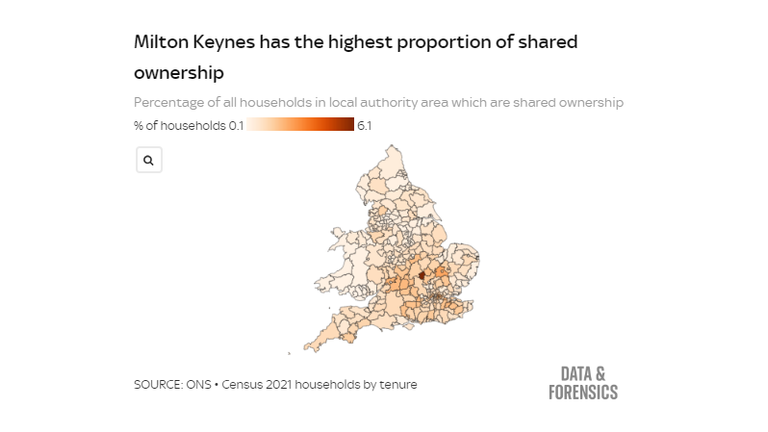

Shared ownership makes up a relatively small percentage of households overall, at around one in 100 according to the latest Census data – with slightly higher concentrations in some areas, mostly in the south of England.

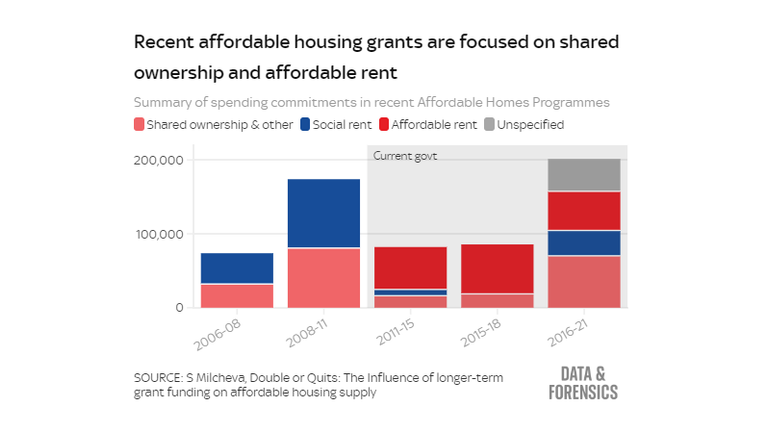

However, it does now make up a half of new funding spent on affordable housing, overtaking social rent as the main type of publicly subsidised housebuilding under the current government.

The main types of affordable housing tenures are social rent, affordable rent (which is less subsidised than social rent, at up to 80% of market rates) and shared ownership.

There has been more incentive for developers – who often have a quota of affordable housing to meet set by local authorities – to build shared ownership or affordable rent properties.

The Affordable Homes Programme, which has been the primary funding source for new affordable homes since 2011, has also switched focus away from social rent towards shared ownership and affordable rent.

This trend continued in the latest funding commitment for 2021-2026, with 50% of the £11.5bn allocated for 162,000 new affordable homes earmarked for shared ownership, with the other 50% split between social rent and affordable rent.

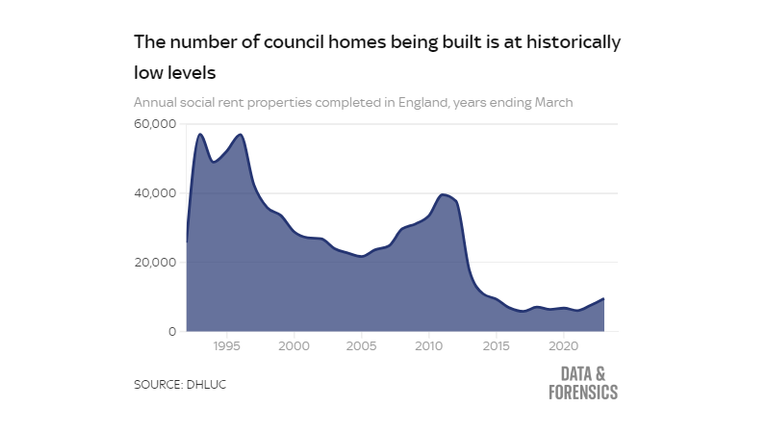

As a result of the lack of incentive to build social rent properties, the number of new builds is at historically very low levels with less than 10,000 completed in 2022/23.

A DLUHC spokesperson said: “Through our long-term plan for housing, we are investing £11.5bn in the Affordable Homes Programme and remain on track to build one million over this Parliament.

“Shared ownership has a vital role to play in helping people onto the property ladder, and since 2010 we have delivered approximately 156,800 new shared ownership homes.”

They said they are taking action to ensure the shared ownership scheme provides the best value for owners, including proposals to give the right to extend leases by 990 years in the Leasehold and Freehold Reform Bill.

“I feel bad pushing the problems onto someone else, but I want to get out”

The Levelling Up, Housing and Communities Committee‘s (LUHCC) cross-parliamentary report noted as well as the issues of rising rents and uncapped service charges, shared owners have “a disproportionate exposure to repair and maintenance costs”.

Despite improvements to shared ownership leases from 2021, with the introduction of a 10-year period for repairs, they say more can be done to make costs proportionate to the size of share owned, including proportional service charges as well maintenance costs.

“Then the housing association will have ‘skin in the game’ and might be incentivised to better scrutinise service charges and property management companies,” said Prof Milcheva.

Shared ownership homes in Colchester

Meanwhile, owners of earlier contracts remain responsible for 100% of costs, regardless of if the property has changed hands.

This creates a “two tier” system, where older properties become unattractive and harder to sell, according to the report.

Will Eggleston, a 33-year-old metalworker bought 50% of his Southwest London flat in 2019.

His service charge has more than doubled since then, from £200 to over £400 a month, with most of the increase happening in the past year.

“There’s just no visible benefit and no explanation to it. The building is in worse condition than when I moved in. The garden has died, the hall is in a bad state,” he said.

His building is one of many high rises to have been impacted by cladding safety concerns and costs of remediation following the 2017 Grenfell Tower fire tragedy.

“L&Q – who are my head lease, hadn’t mentioned anything about cladding or anything when I was purchasing the flat,” said Mr. Eggleston.

This can be a particular issue for shared owners with covenants that prevent them subletting properties they can no longer afford to live in at market rates.

A spokesperson for L&Q said: “L&Q is a charitable housing association and does not make profits from service charges.”

Kinleigh Folkard & Hayward (KFH), the property managers at Mr Eggleston’s building, said that the doubled service charge is due to increases in general maintenance and cleaning, insurance, electricity, and reserve funds for future works.

They added that they would have made the resident aware of the facts known about cladding at the time he purchased his apartment.

Activist group End Our Cladding Scandal say the government and housing providers have failed to mitigate the impact of the building safety crisis on shared owners.

They said: “This has already led to repossessions and forced shared owners into distressed sales to cash buyers.

“Others have had to become “accidental landlords”, forced into loss-making subletting agreements while their neighbours, who are private leaseholders, can rent out their flats at whatever rate they choose.”

Meanwhile, the high service charges and ongoing cladding issues are getting in the way of Mr Eggleston’s hopes to sell and move out.

“I feel bad pushing the problems onto someone else. But on the other hand, I want to get out,” he said.

Calls for more transparency

Shared ownership can have a positive role for those who do not qualify for other government affordable homes schemes but cannot access full ownership, being on average cheaper than private renting, according to Prof Milcheva and colleagues’ research.

But there are some key data gaps, including on how common it is for people to staircase up to higher shares of ownership, which make it hard to assess the overall success of the scheme.

Rhys Moore, executive director of public impact at the National Housing Federation, said: “Shared ownership remains an important route to home ownership for many households and we support measures to improve residents’ experience through greater transparency around costs and improved access to information, as well as better government data on the product.”

Ann Santry, chair of Shared Ownership Council said: “We acknowledge the need for further reforms of the tenure to help shared ownership fulfil its potential as an affordable home ownership model.”

Josie Dunn’s bill, including charges for non-existent services like CCTV

In Josie Dom’s case, after being contacted by Sky News her building’s Housing Association Peabody said it had made a mistake and would be issuing a correction letter to residents.

A spokesperson for Peabody said: “It’s important to us that service charges are accurate and reasonable. This was an error and we’re really sorry. No one has been overcharged and we’ve written to those affected.”

At the time of publication, the issue remains unresolved, and residents have not yet received this information.

Josie is in rent arrears. “It’s a crazy amount of stress to go through,” she said.

With additional reporting and production by Michelle Inez Simon, visual investigations producer, and Tom Cheshire, Data & Forensics correspondent

In a small town in Suffolk, a team of police officers walk into a Turkish barbershop.

It’s clean and brightly painted, the local football team’s shirt displayed on one wall. Two young men, awaiting customers, hair and beards immaculate, tell officers they commute to work here from London.

Step through the door at the back of the shop and things look very different.

In a dingy stairwell, a bed has been crammed on to a landing, and a sofa just big enough to sleep on is squeezed under the stairs. The floor and steps are covered with empty pizza boxes, food containers and drink bottles. There’s a pair of socks on the floor and a T-shirt on the bed. An unopened prescription sits on a table.

At least one person is clearly living here, but possibly not by choice.

“This could be linked to exploitation, this could be linked to some forms of modern slavery,” says John French, the modern slavery vulnerability advisor for Suffolk Constabulary.

“You have to ask yourself when you come across this sort of situation, why would someone want to live in these sorts of conditions?”

John French speaks to Paul Kelso

Behind a second door, this one padlocked, is a second room. This one cleaner, but clearly not safe.

Phrases in Turkish and English have been scribbled on post-it notes stuck to the wall and officers find a driving licence with a local address.

“Judging by the state of the room, this could be an ‘Alpha’ living in here,” says Mr French.

“An ‘Alpha’ is someone who’s previously been exploited,” he explains. “They have been given a little bit of trust and act like a kind of supervisor. They are very important to us, because we want to get them away from others before they can influence them.”

A brand-new Audi SUV is parked at the back.

What’s going on here?

We are in Haverhill, a small town in Suffolk bypassed by the rail network and the prosperity enjoyed elsewhere in the county, its central street bearing the familiar markers of town-centre decline.

There’s a Costa, a Boots, a branch of Peacocks, and several pubs and cafes, but they’re punctuated by “cash intensive” businesses including barbers, vape stores and takeaways, and several vacant premises that stand out like missing teeth.

It’s the cash intensive businesses that have brought the attention of police, these local raids part of the National Crime Agency’s (NCA’s) Operation Machinize, targeting money laundering, criminality and immigration offences hidden in plain sight on high streets across England.

There are 17 premises of interest in Haverhill alone, among more than 2,500 sites visited since the start of October, resulting in 924 arrests and more than £2.7m of contraband seized.

In a single block of five shops on the High Street, four are raided. A sweet shop yields a haul of smuggled cigarettes stashed in food delivery boxes.

In the Indian restaurant three doors down a young Asian man is interviewed via an interpreter dialling in on an officer’s phone. They establish his student visa has been revoked, and he has had a claim for asylum rejected.

The aim is to disrupt criminality using any means possible, be they criminal or civil. Criminal or not, the living conditions at the barbers are likely to fall foul of planning and building regulations enforceable with penalties including fines and closure, so officials from the council and fire safety are on hand.

Trading Standards are here to handle counterfeit goods seizures, and immigration officers are on hand to check the status of those questioned, pursuing anyone without permission to be in the UK.

UK could use Denmark’s immigration model

‘A full spectrum of criminality’

Sal Melki, the NCA’s deputy director of financial crime, explains why the agency is targeting apparently small operations.

“We’re finding everything from the laundering of millions of pounds into high value goods like really expensive watches, through to the illicit trade of tobacco and vapes, and people that have been trafficked into the country working in modern slavery conditions. We’re seeing a full spectrum of criminality.

“We want to disrupt them with seizures, arrests, and prosecutions and make sure bad businesses are replaced with successful, thriving businesses that make us all feel safer and more prosperous.”

Read more from Sky News:

British journalist held in US to be freed

Reeves all but admits tax rises to come

The last visit is to a small supermarket. Through the back door is another hidden bedroom, this one not much larger than a broom cupboard, with a makeshift bed made from a sheet of plywood and a duvet.

The man behind the counter, who says he’s from Brazil via Pakistan, claims not to live in the shop, but his luggage is in a storeroom. He’s handcuffed and questioned by immigration officers, and admits working illegally on a visitor visa.

“If he is proven to be working illegally he’ll be taken to a detention centre and administratively removed,” an immigration officer tells me. “That’s not the same as deportation, the media always gets that wrong. He’ll be given the chance to book his own ticket, and if not, he’ll be removed.”

Shortly afterwards he’s put in a police car, his large red suitcase squeezed onto the front seat, and driven away.

The Post Office has agreed a further extension to its scandal-hit software deal with the Japanese company Fujitsu as it plots a move to a rival supplier in the next couple of years.

Sky News has learnt that the Post Office, which is owned by the government, is to pay another £41m to Fujitsu for the use of the Horizon system from next April until 31 March 2027.

The move comes as Post Office bosses prepare to sever the company’s partnership with Fujitsu, which is under pressure to pay hundreds of millions of pounds for its part in the scandal.

Money latest: BA partnership with Musk’s Starlink

Hundreds of sub-postmasters were wrongfully imprisoned for fraud and theft because of flaws with Fujitsu’s software, which it subsequently emerged were suspected by executives involved in its management.

Last week, Sky News revealed that Sir Alan Bates, who led efforts to seek justice for the victims of what has been dubbed Britain’s biggest miscarriage of justice, had settled his multimillion pound compensation claim with the government.

Sir Alan received a seven-figure sum, which one source said may have amounted to between £4m and £5m.

Alan Bates: New redress scheme ‘half-baked’

In a statement issued in response to an enquiry from Sky News, a Post Office spokesperson said: “The Post Office has agreed with Fujitsu a one-year bridging extension to the Horizon contract for the period 1 April 2026 to 31 March 2027.

“We are committed to moving away from Fujitsu and off the Horizon system as soon as possible.

“We are bringing in a different supplier to take over Horizon whilst a new system is developed, and this process is well underway.

“We expect to award a contract for a new supplier to manage Horizon by July 2026, according to current timelines.”

Will Post Office victims be cleared?

Fujitsu executives have acknowledged that the company has a “moral obligation” to contribute financially as a result of the Horizon scandal, but has yet to agree a final figure with the government.

It is said to be unlikely to do so until the conclusion of Sir Wyn Williams’ public inquiry.

The Department for Business and Trade has been contacted for comment.

Former Tesco boss Sir Dave Lewis is to become the new chief executive of Diageo, the struggling FTSE 100 drinks giant.

The world’s largest spirits maker, which counts Guinness and Johnnie Walker whisky among its stable of brands, said he would assume the role in January.

The search for a new boss began in July when Debra Crew was effectively ousted after two years in charge.

Money latest: BA partnership with Musk’s Starlink

The company’s share price fell 40% during her tenure as the industry grappled a drastic decline in the number of people drinking at home following the COVID pandemic and, more recently, the US trade war.

A planned fightback by Ms Crew was seen by investors as failing to go far enough.

Sir Dave led a six-year turnaround of Tesco, the UK’s biggest retailer, from 2014.

He earned the nickname ‘Drastic Dave’ in his previous role at Unilever, the consumer goods giant, where he was credited with achieving similar success through cost-cutting and targeted marketing.

Diageo’s market positions have fared better than rivals during the downturn but its shares are still hovering around lows not seen for a decade.

Debra Crew was appointed chief executive after the sudden death of Sir Ivan Menezes in 2023. Pic: Diageo

Only last week, the company downgraded its sales and profit outlook for next year.

Diageo chair John Manzoni told investors: “The Board unanimously felt that Dave has both the extensive CEO experience, and the proven leadership skills in building and marketing world-leading brands, that is right for Diageo at this time.”

Sir Dave said of the task facing him: “Diageo is a world leading business with a portfolio of very strong brands, and I am delighted to be joining the team.

“The market faces some headwinds but there are also significant opportunities. I look forward to working with the team to face these challenges and realise some of the opportunities in a way which creates shareholder value.”

Diageo shares were 7% up on news of the appointment.

Matt Britzman, senior equity analyst at Hargreaves Lansdown, responded: “Lewis brings deep experience in consumer brands from his time leading Tesco and decades at Unilever, though he lacks direct exposure to the spirits industry.

“Investors may welcome his strong marketing pedigree, but any major strategic reset will take time, leaving near-term focus on navigating tough trading conditions.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024