Rachel Reeves defends decision not to restore bankers’ bonus cap

Rachel Reeves has defended her decision not to restore a cap on bankers’ bonuses, arguing businesses do not need “more chopping and changing”.

The shadow chancellor said that when the government scrapped the cap under Liz Truss, Labour did not “feel that was the right priority in that budget”.

But she said much stronger rules were now in place since the 2008 financial crash, when the cap was first introduced, and that it was no longer her priority to restore it.

“What I hear loud and clear from business is that what it will take to get them to invest in Britain is stability and the last thing they need is more chopping and changing,” she said.

“The chopping and changing has got to end if we’re going to give stability to business and that’s why we will not be bringing that back.”

Politics latest:

Labour ‘under no illusions about scale of task ahead’

Shadow chancellor Rachel Reeves addressing 400 business leaders at the Kia Oval on 1 February 2024. Pic: PA

Addressing Labour’s business conference in central London this morning, Ms Reeves also announced she would not increase the headline rate of corporation tax of 25% during the first term of a Labour government but left the door open to changes in the rate in the future.

She said: “There have been 26 changes to our corporation tax arrangements in this parliament alone. We can’t go on like this.

“The next Labour government will make the pro-business choice and the pro-growth choice: We will cap the headline rate of corporation tax at its current rate of 25% for the next parliament.

“And should our competitiveness come under threat, if necessary we will act.”

Ms Reeves also said Labour would maintain full expensing and the annual investment allowance and would provide a “road map” for business taxation within the first six months of government.

Ms Reeves has sought to portray herself as pro-business during her time as shadow chancellor, in contrast to her predecessor John McDonnell, who led Labour’s economic policy when Jeremy Corbyn was the leader of the Opposition.

Will Labour stick to £28bn a year green pledge?

However, the shadow chancellor is facing scrutiny over Labour’s pledge to spend £28bn a year on green projects until 2030 if the party comes into power.

In a Q&A following her speech, Ms Reeves failed to commit to the policy, which some in Labour want Sir Keir Starmer to drop because it allows the Conservatives to cast doubt on the party’s commitment to fiscal discipline.

Asked by Sky News’s political editor Beth Rigby whether the pledge had become “an albatross around your neck” that “threatens to unravel all the hard work you’ve done to be trusted with economic competence”, Ms Reeves said there were “big opportunities to invest alongside business in the jobs and the industries of the future”.

Will Labour spend £28bn?

But she said it was “absolutely essential that all of our policies are consistent with our fiscal rules” and that the green prosperity plan “was no exception to that”.

The shadow chancellor said that after the next budget, the party will “set out our plans and ensure they are consistent with our fiscal rules because they will always take precedence to guarantee the economic security of family finances and of businesses as well”.

Sir Keir Starmer and Rachel Reeves during a visit to the London Stock Exchange Group last year. Pic: PA

Tories attack Labour over bonus cap change

The cap on bankers’ bonuses was first introduced in the wake of the 2008 financial crisis to limit annual payouts to twice a banker’s salary, but it was scrapped by former chancellor Kwasi Kwarteng during Ms Truss’s short time as prime minister.

During Prime Minister’s Questions this week, Rishi Sunak seized on the issue to argue that voters “cannot trust a word he [Sir Keir Starmer] says”.

“I was genuinely surprised that, after recently and repeatedly attacking not just me but the government for lifting the bonus cap, the shadow chancellor has announced, just today, that she now supports the government’s policy on the bankers’ bonus cap.”

Read more:

Starmer promises to ‘fix stagnation’ in pitch to business

Labour reports to underpin new ‘party of business’ stance

Sunak: ‘It’s the same old Labour party’

Ms Reeves and other senior Labour figures had been vocal critics of the government’s decision to axe the cap during a cost of living crisis, saying only three months ago that the decision to allow unlimited bonuses to be earned again “tells you everything you need to know about this government”.

The issue has caused some division within Labour, with Anas Sarwar, the party’s leader in Scotland, previously criticising Ms Truss as a “Thatcher tribute act” who would rather “boost bankers’ bonuses than help those in need”.

He told reporters in Westminster today that he stood by his previous words but added: “You have got to look at it in the balance. We have got to inspire confidence for them to make the strategic investments, but we can’t return to a situation where they get away with it.

“I’m not here to defend bankers’ bonuses, I’m not here to defend banks. That is something the UK Treasury has got to keep an eye on.”

Stephen Flynn, the SNP’s leader in Westminster and Labour’s main opponent in Scotland, sarcastically praised Mr Sunak for convincing the Labour Party to agree to a “bleak future”, saying it was a “great achievement” for the government.

Business

US trade war: The state of play as Trump signs order imposing new tariffs – but there are more delays

Donald Trump’s trade war has been difficult to keep up with, to put it mildly.

For all the threats and bluster of the US election campaign last year to the on-off implementation of trade tariffs – and more threats – since he returned to the White House in January, the president‘s protectionist agenda has been haphazard.

Trading partners, export-focused firms, customs agents and even his own trade team have had a lot on their plates as deadlines were imposed – and then retracted – and the tariff numbers tinkered.

Money latest: Why your internet feels slower

While the UK was the first country to secure a truce of sorts, described as a “deal”, the vast majority of nations have failed to secure any agreement.

Deal or no deal, no country is on better trading terms with the United States than it was when Trump 2.0 began.

Here, we examine what nations and blocs are on the hook for, and the potential consequences, as Mr Trump’s suspended “reciprocal” tariffs prepare to take effect. That will now not happen until 7 August.

What does the UK-US trade deal involve?

Why was 1 August such an important date?

To understand the present day, we must first wind the clock back to early April.

Then, Mr Trump proudly showed off a board in the White House Rose Garden containing a list of countries and the tariffs they would immediately face in retaliation for the rates they impose on US-made goods. He called it “liberation day”.

The tariff numbers were big and financial markets took fright.

Just days later, the president announced a 90-day pause in those rates for all countries except China, to allow for negotiations.

The initial deadline of 9 July was then extended again to 1 August. Late on 31 July, Mr Trump signed the executive order but said that the tariff rates would not kick in for seven additional days to allow for the orders to be fully communicated.

Since April, only eight countries or trading blocs have agreed “deals” to limit the reciprocal tariffs and – in some cases – sectoral tariffs already in place.

Who has agreed a deal over the past 120 days?

The UK, Japan, Indonesia, the European Union and South Korea are among the eight to be facing lower rates than had been threatened back in April.

China has not really done a deal but it is no longer facing punitive tariffs above 100%.

Its decision to retaliate against US levies prompted a truce level to be agreed between the pair, pending further talks.

There’s a backlash against the EU over its deal, with many national leaders accusing the European Commission of giving in too easily. A broad 15% rate is to apply, down from the threatened 30%, while the bloc has also committed to US investment and to pay for US-produced natural gas.

Millions of EU jobs were in firing line

Where does the UK stand?

We’ve already mentioned that the UK was the first to avert the worst of what was threatened.

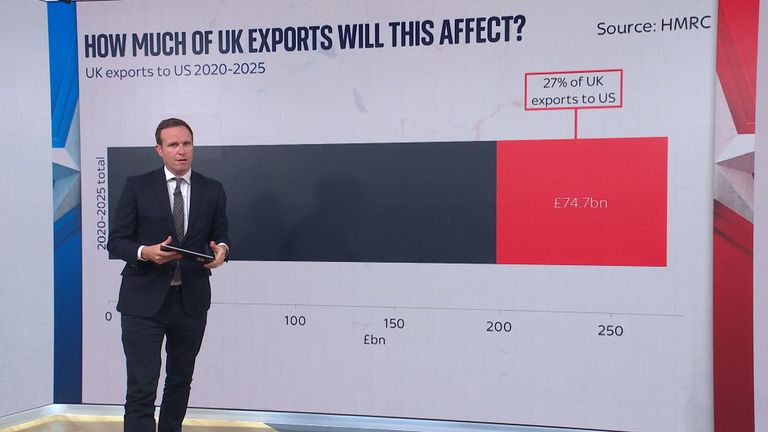

While a 10% baseline tariff covers the vast majority of the goods we send to the US, aerospace products are exempt.

Our steel sector has not been subjected to Trump’s 50% tariffs and has been facing down a 25% rate. The government announced on Thursday that it would not apply under the terms of a quota system.

UK car exports were on a 25% rate until the end of June when the deal agreed in May took that down to 10% under a similar quota arrangement that exempts the first 100,000 cars from a levy.

Who has not done a deal?

Canada is among the big names facing a 35% baseline tariff rate. That is up from 25% and covers all goods not subject to a US-Mexico-Canada trade agreement that involves rules of origin.

America is its biggest export market and it has long been in Trump’s sights.

Mexico, another country deeply ingrained in the US supply chain, is facing a 30% rate but has been given an extra 90 days to secure a deal.

Brazil is facing a 50% rate. For India, it’s 25%.

What are the consequences?

This is where it all gets a bit woolly – for good reasons.

The trade war is unprecedented in scale, given the global nature of modern business.

It takes time for official statistics to catch up, especially when tariff rates chop and change so much.

Any duties on exports to the United States are a threat to company sales and economic growth alike – in both the US and the rest of the world. Many carmakers, for example, have refused to offer guidance on their outlooks for revenue and profits.

Apple warned on Thursday night that US tariffs would add $1.1bn of costs in the three months to September alone.

Barriers to business are never good but the International Monetary Fund earlier this week raised its forecast for global economic growth this year from 2.8% to 3%.

Some of that increase can be explained by the deals involving major economies, including Japan, the EU and UK.

US growth figures have been skewed by the rush to beat import tariffs.

Read more:

Trump signs executive order for reciprocal tariffs

Aston Martin outlines plan to ease US tariff hit

The big risk ahead?

It’s a self-inflicted wound.

The elephant in the room is inflation. Countries imposing duties on their imports force the recipient of those goods to foot the additional bill. Do the buyers swallow it or pass it on?

The latest US data contained strong evidence that tariff charges were now making their way down the country’s supply chains, threatening to squeeze American consumers in the months ahead.

It’s why the US central bank has been refusing demands from Mr Trump to cut interest rates. You don’t slow the pace of price rises by making borrowing costs cheaper.

A prolonged period of higher inflation would not go down well with US businesses or voters. It’s why financial markets have followed a recent trend known as TACO, helping stock markets remain at record levels.

The belief is that Trump always chickens out. He may have to back down if inflation takes off.

It is “Liberation Day” III – the third tariff deadline set by Donald Trump.

Countries without bilateral trade agreements will soon face reciprocal tariffs – ranging from 25% to 50% – with a baseline of 15% to 20% for any not making a deal.

He has delayed twice, from April to July and from July to August, but hammered this date home in his trademark caps-on style: “THE AUGUST FIRST DEADLINE STANDS STRONG, AND WILL NOT BE EXTENDED. A BIG DAY FOR AMERICA!!!”

“Will not be extended” for anyone but Mexico, it seems. The country secured a 90-day extension at the last minute, with Mr Trump citing the “complexities” of the border.

Explained: The US-UK trade deal

By close of business on the eve of deadline, he had a handful of framework deals – some significant – including the UK (10%), the EU, Japan and South Korea (15%), Indonesia and the Philippines (19%), Vietnam (20%).

On the EU agreement, which he struck in Scotland, the president said: “It’s a very powerful deal, it’s a big deal, it’s the biggest of all the deals.”

But what happened to the “90 deals in 90 days” touted by the White House earlier this year?

The short answer is they were replaced by letters of instruction to pay a tariff set by the US.

How Trump 2.0 changed the world

Amid of flurry of late activity, the US played hardball with major trading partners like Canada.

“For the rest of the world, we’re going to have things done by Friday,” said US Commerce Secretary Howard Lutnick – the “rest of the world” meaning everyone but China.

There is, apparently, the “framework of a deal” between the world’s two largest economies, but talks between Washington and Beijing are continuing.

Read more US news:

Top Trump officials to visit Gaza

Heavy rain and flash floods batter east coast

Worker begs America for help

In terms of wins, he can claim some significant deals and point to his tariffs having generated an impressive $27bn (£20.4bn) in June, not bad for a single month.

But the legality of the approach is under siege – with the US Court of International Trade ruling that the “Liberation Day” tariffs exceeded the president’s authority, with enforcement paused pending appeal.

The deadline has stirred the pot, forcing a handful of deals onto the table. Whether they stick or survive legal scrutiny is far from settled.

But the playbook remains the same – threaten the world with trade chaos, whittle it down, celebrate the wins, and pray no one checks what’s legal.

Microsoft has become only the second publicly traded company after Nvidia to surpass $4 trn (£3.03trn) in market valuation, after registering huge earnings.

On Thursday, shares rose on Wall Street with the S&P 500 and Nasdaq climbing to new record highs.

Stocks in Microsoft jumped after posting better-than-expected results, helped by its Azure cloud computing platform, which is a centrepiece of the company’s artificial intelligence (AI) efforts.

Shares in Facebook and Instagram’s parent company, Meta, also surged after beating sales and profit targets.

Is Trump’s AI plan a ‘tech bro’ manifesto?

Technology giants Apple and Amazon will report their results after Wall Street’s close.

Microsoft first cracked the $1trn (£760bn) mark in April 2019, but its move to $3trn (£2.27trn) took longer than technology giants Nvidia and Apple.

Nvidia tripled its value in just about a year and clinched the $4trn milestone before any other company on 9 July. Apple was last valued at $3.12trn.

In comparison, the biggest UK company by market value is drug manufacturer AstraZeneca, worth $235.97bn (£178.55bn).

Companies ranked by market value (USD), according to tradingview.com

1. Nvidia (US) $4.43trn

2. Microsoft (US) $4trn

3. Apple (US) $3.12trn

4. Amazon (US) $2.47trn

5. Alphabet (US) $2.35trn

6. Meta (US) $1.95trn

7. Saudi Arabian Oil (Saudi Arabia) $1.56trn

8. Broadcom (US) $1.42trn

9. Berkshire Hathaway (US) $1.03trn

10. Tesla (US) $1.02trn

11. Taiwan Semiconductor Manufacturing (Taiwan) $1trn

29. Samsung Electronics (South Korea) $338.06bn

36. Alibaba (China) $284.62bn

52. AstraZeneca (UK) $235.97bn

While sweeping US tariffs had investors worried about tighter business spending, Microsoft’s strong earnings have shown that the company’s books are yet to take a hit.

Microsoft’s multibillion-dollar bet on OpenAI is proving to be a game changer, powering its Office Suite and Azure offerings with cutting-edge AI and fueling the stock to more than double its value since ChatGPT’s late-2022 debut.

Listen to The World with Richard Engel and Yalda Hakim every Wednesday

Read more from Sky News:

Microsoft beats Nvidia by market value

Trump unveils AI action plan

UK ramps up AI adoption with Meta

On Wednesday, the firm announced Azure sales surpassed $75bn (£56bn) on an annual basis, while Azure revenue jumped 39% in the April-June quarter.

Overall revenue rose 18% to $76.4bn (£57.81bn) over the same period.

It is also forecasting a record $30bn (£22.7bn) in capital spending over the first quarter to meet soaring AI demand..

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike