UnitedHealth Group has paid more than $3 billion to providers following cyberattack

In this photo illustration the UnitedHealth Group logo displayed on a smartphone screen.

Sheldon Cooper | Sopa Images | Lightrocket | Getty Images

UnitedHealth Group has paid out an additional $1 billion to providers that have been impacted by the Change Healthcare cyberattack since last week, bringing the total amount of funds advanced to more than $3.3 billion, the company said on Wednesday.

UnitedHealth, which owns Change Healthcare, discovered in February that a cyber threat actor had breached part of the unit’s information technology network. Change Healthcare processes more than 15 billion billing transactions annually, and one in every three patient records passes through its systems, according to its website.

The company disconnected the affected systems “immediately upon detection” of the threat, according to a filing with the SEC. The interruptions left many health-care providers temporarily unable to fill prescriptions or get reimbursed for their services by insurers.

Many health-care providers rely on reimbursement cash flow to operate, so the fallout has been substantial. Smaller and mid-sized practices told CNBC they were making tough decisions about how to stay afloat. A survey published by the American Hospital Association earlier this month found that 94% of hospitals have experienced financial disruptions from the attack.

As a result, UnitedHealth introduced its temporary funding assistance program to help providers in need of support. The company said the $3.3 billion in advances will not need to be repaid until claims flows return to normal. Federal agencies like the Centers for Medicare & Medicaid Services have introduced additional options to ensure that states and other stakeholders can make interim payments to providers, according to a release.

UnitedHealth has been working to restore Change Healthcare’s systems in recent weeks, and it expects some disruptions will continue into April, according to its website. The company began processing a backlog of more than $14 billion in claims on Friday, and on Wednesday said, “claims have begun to flow.”

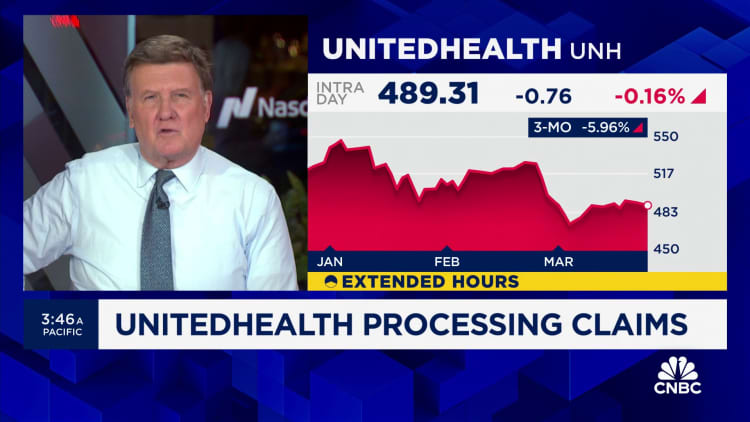

Shares of UnitedHealth have fallen more than 6% since the attack was disclosed.

Late last month, the company said the ransomware group Blackcat is behind the attack. Blackcat, also called Noberus and ALPHV, steals sensitive data from institutions and threatens to publish it unless a ransom is paid, according to a December release from the U.S. Department of Justice.

The Department of State on Wednesday announced it’s offering a reward of up to $10 million for information that could help identify or locate cyber actors linked to Blackcat.

UnitedHealth said Wednesday that it’s “still determining the content of the data that was taken by the threat actor.” The company said a “leading vendor” is analyzing the impacted data. United Health is working closely with law enforcement and third parties like Palo Alto Networks and Google‘s Mandiant to assess the attack.

“We continue to be vigilant, and to date have not seen evidence of any data having been published on the web,” UnitedHealth said. “And we are committed to providing appropriate support to people whose data is found to have been compromised.”

Rep. Jamie Raskin, D-Md., ranking member of the House Committee on Oversight and Accountability, wrote a letter to UnitedHealth CEO Andrew Witty on Monday requesting information about the “scope and extent” of the breach.

Raskin asked Witty for information about when Change Healthcare notified its clients about the breach, what specific infrastructure and information was targeted and what cybersecurity procedures the company has in place. The committee requested written responses “no later” than April 8.

“Given your company’s dominant position in the nation’s health care and health insurance industry, Change Healthcare’s prolonged outage as a result of the cyberattack has already had ‘significant and far-reaching’ consequences,” Raskin wrote.

The Biden administration also launched an investigation into UnitedHealth earlier this month due to the “unprecedented magnitude of the cyberattack,” according to a statement.

WATCH: UnitedHealth unit begins processing $14 billion medical claims backlog

Sopa Images | Lightrocket | Getty Images

Google on Thursday rolled out Nano Banana Pro, its latest image editing and generation tool, continuing the company’s momentum after launching its new Gemini artificial intelligence model earlier this week.

The product is built on Gemini 3 Pro, which was announced on Tuesday and contributed to record-breaking stock highs.

Alphabet’s stock was up 4% Thursday.

Josh Woodward, vice president of Google Labs and Gemini, told CNBC’s Deirdre Bosa that the Nano Banana Pro’s capabilities expand beyond its original iteration, which launched in late August.

“It’s incredible at infographics. It can make slide decks. It can take up to 14 different images, or five different characters, and sort of keep that character consistency,” he said.

He added that internal users have experimented with the feature by inputting code snippets and even LinkedIn resumes to create infographics.

“I think this ability to visualize things that were previously maybe not something you would think of as a visual medium that tends to be one of the magic things people are finding with it,” Woodward said.

The original Nano Banana went viral on social media as users turned photos of themselves or their pets into hyperrealistic 3D figurines. Woodward wrote in an X post in September that the product helped add 13 million new users to the Gemini app in the span of four days.

Nano Banana Pro is currently available in the Gemini app, with limited free quotas, Google’s writing assistant, NotebookLM, as well as the company’s developer, enterprise and advertising products.

Google AI Pro and Ultra subscribers will have access to the product in Google’s search features AI Mode.

The feature will later also roll out to Ultra subscribers first in Flow, Google’s AI filmmaking tool.

Google introduced another feature in the Gemini app that allows users to upload any image to find out if it was generated by Google AI.

Images generated on free Nano Banana accounts will have a watermark, but it will be removed for Google AI Ultra tier subscribers.

Google has been working to gain ground on OpenAI in the generative AI race, which ignited after the release of ChatGPT in 2022.

Last week, OpenAI announced two updates to its GPT-5 model to make it “warmer by default and more conversational” as well as ” more efficient and easier to understand in everyday use,” the company said.

ChatGPT currently tops the list of free apps on Apple’s App Store, with Gemini in the second spot.

The Gemini app currently has over 650 million monthly active users per month, and Gemini-powered AI Overviews has 2 billion monthly users, Google said in a release. OpenAI CEO Sam Altman said in October that ChatGPT had reached 800 million weekly active users.

Woodward said Google AI products have had growing demand, with many users signing up for Gemini’s subscription plan to have “higher limits with some of these advanced models.”

“We’re seeing high numbers of people coming to lots of these products,” he said. “That’s really the best problem to have, is there’s a lot of demand, and we’re trying to figure out actually how to serve it.”

The company is looking to continue scaling its AI offerings, Woodward said, highlighting Flow, Google’s AI filmmaking tool, and Genie, a “world building” model that is currently available as a limited research preview.

Technology

U.S. greenlights AI chip exports to Gulf tech giants after Saudi Crown Prince’s Washington visit

U.S. President Donald Trump and Crown Prince and Prime Minister Mohammed bin Salman of Saudi Arabia stand for a photo with Tesla CEO Elon Musk, Nvidia CEO Jensen Huang and other participants at the U.S.-Saudi Investment Forum at the Kennedy Center on Nov. 19, 2025 in Washington, DC.

Win McNamee | Getty Images

The U.S. has approved sales of advanced Nvidia chips to Saudi Arabia’s HUMAIN and the United Arab Emirates’ G42, authorizing the state-backed firms to buy up to 35,000 chips, worth an estimated $1 billion.

The approval of these chip exports marks a major reversal for the U.S., which had previously balked at the idea of direct exports to state-backed AI companies in the Gulf. Export controls were put into place to avoid advanced American technology making its way to China through the back door of Gulf Arab states.

Before former President Joe Biden left office in January, he administered a final round of export restrictions on advanced AI chips, targeting companies like Nvidia, in a sweeping effort to keep that cutting-edge U.S. intellectual property out of China’s reach.

Now, President Donald Trump is moving to expand the reach of such advanced technology in order to “promote continued American AI dominance and global technological leadership,” the U.S. Commerce Department said in a statement published on Wednesday.

The U.S. Commerce Department approved the chip exports, with the condition the state-backed AI outfits agree to “rigorous security and reporting requirements,” overseen by the Department of Commerce’s Bureau of Industry and Security.

Saudi’s Victory Lap

The export approval follows Saudi Crown Prince Mohammed bin Salman’s trip to Washington this week where the Kingdom pledged to spend $1 trillion in the U.S., up from $600 billion originally committed during Trump’s Gulf tour in May.

“Even if we don’t get to that, both sides have skin in the game,” Afshin Molavi, senior fellow at the Foreign Policy Institute of the Johns Hopkins University School of Advanced International Studies, told CNBC’s Dan Murphy.

Saudi Arabia’s AI company HUMAIN, backed by its nearly $1 trillion Public Investment Fund signed a long list of partnerships with Adobe, Qualcomm, AMD, Cisco, GlobalAI, Groq, Luma, and xAI at a U.S.-Saudi Investment Forum held in Washington, D.C this week. Notably, HUMAIN will be teaming up with Elon Musk’s xAI to build a 500 megawatt data center in the Kingdom.

“What we want to do in 2026 is to build the capacity equivalent to what Saudi has built in the last 20 years, in one year,” Tareq Amin, CEO of HUMAIN, said at the summit. HUMAIN is hoping to position Saudi Arabia as the third biggest global AI hub, after the likes of the U.S. and China.

Winning over the U.S. Commerce Department

Saudi Arabia’s HUMAIN and UAE’s G42 “have the capital to invest, the relationships with Nvidia and the (relationship with the) U.S. government,” Kamil Dimmich, partner and portfolio manager at North of South Capital, told CNBC’s Dan Murphy in an interview on Wednesday.

G42 and HUMAIN are “able to use this to build out regional infrastructure, and they want to leverage that infrastructure to become a global hub for compute,” Dimmich added.

Just two weeks ago, Microsoft secured an export license for advanced chips to the UAE. Microsoft’s key partner in the UAE is G42, but the local AI company was notably absent from the Microsoft announcement, until today.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024