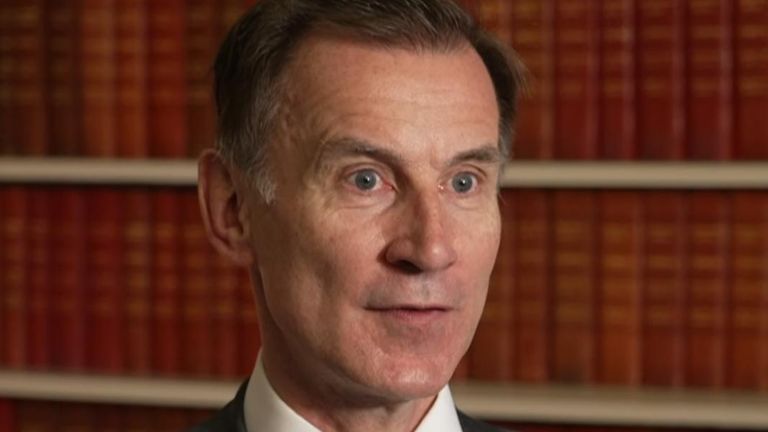

Chancellor Jeremy Hunt insists UK’s economy has ‘turned corner’ – telling public to ‘stick to plan’ for ‘better times’

Chancellor Jeremy Hunt has said that “better times are ahead” but that the fundamentals of the UK economy are “very strong”.

Speaking to Sky News in Washington, Mr Hunt pointed to price rise data from today showing a drop in the rate of inflation as well as the latest jobs figures and IMF economic growth predictions.

Money latest:

Tourist tax warning in 10 European cities

Mr Hunt said: “I think the economy, we are seeing, has turned the corner, people are beginning to feel that.”

“That will continue during the course of this year. But the fundamentals for the UK economy, yes, are very strong indeed,” he added.

The cost of living crisis, brought about by months of double-digit inflation last year, has been tough, Mr Hunt said.

But sticking to his economic plan, along with the Bank of England’s work to control interest rates, will bring about “better times”, he insisted – in a sign of the likely economic messaging from the Tories ahead of the coming general election.

Jeremy Hunt urged the public to ‘stick to the plan’

“If we stick to that plan we can see that we will have better times ahead,” he said.

He added: “We don’t pretend that it hasn’t been tough, it’s been very tough in the UK and in many other countries.

“We now have the biggest technology industry in Europe. That is a big positive for families up and down the country in the years ahead.”

A whiff of wishful thinking about Hunt’s declaration of economic ‘soft landing’

It’s not quite a Mission Accomplished moment – the equivalent of that day in 2003 when George W Bush stood on an aircraft carrier and prematurely declared the Iraq war was over.

But Jeremy Hunt’s declaration in our interview in Washington that he had achieved a “soft landing” in the economy certainly has a whiff of wishful thinking about it.

The chancellor was at pains to insist today that in fact the outlook is strikingly positive.

Of course, that confidence comes as he gears up for an election in which the economy is likely to be centre stage.

Yet the chancellor is not alone in clinging to optimism.

Here in Washington, most central bankers and finance ministers are quietly hoping that all the economic and military challenges facing them do not crystallise.

They, like Jeremy Hunt, would much rather keep on talking about soft landings.

Sanctions warning for Iran

When asked about sanctions on Iran, following its strikes on Israel last weekend, Mr Hunt said he will be pushing for more to be added in his meetings with leaders of the G7 group of nations and with US Treasury Secretary Janet Yellen.

“What I would say is this: The talk ten days ago was of the West drifting away from its support for Israel. But when Iran attacked Israel, Western support was rock solid.

“And if Iran takes action that destabilises the global economy through what it does in the Middle East then they will face a concerted response from Western countries,” he said.

Keep up with all the latest news from the UK and around the world by following Sky News

‘I don’t want to say anything negative about Liz Truss’

Mr Hunt declined to speak ill of former prime minister Liz Truss when asked if she was harming the Conservative Party.

“I think Liz will be the first to accept that during her time as prime minister, mistakes were made,” he said of her 49-day tenure.

During her premiership government borrowing costs soared; the pound hit a 37-year low against the dollar – making imports more expensive; mortgage rates soared and the Bank of England made an unprecedented intervention to stop pension funds collapsing.

“She appointed me as chancellor. And so, you know, I don’t want to say anything negative about Liz Truss,” Mr Hunt said.

Thousands of job cuts at the NHS will go ahead after the £1bn needed to fund the redundancies was approved by the Treasury.

The government had already announced its intention to slash the headcount across both NHS England and the Department of Health by around 18,000 administrative staff and managers, including on local health boards.

The move is designed to remove “unnecessary bureaucracy” and raise £1bn a year by the end of the parliament to improve services for patients by freeing up more cash for operations.

NHS England, the Department of Health and Social Care, and the Treasury had been in talks over how to pay for the £1bn one-off bill for redundancies.

It is understood the Treasury has not granted additional funding for the departures over and above the NHS’s current cash settlement, but the NHS will be permitted to overspend its budget this year to pay for redundancies, recouping the costs further down the line.

‘Every penny will be spent wisely’

Chancellor Rachel Reeves is set to make further announcements regarding the health service in the budget on 26 November.

And addressing the NHS providers’ annual conference in Manchester today, Mr Streeting is expected to say the government will be “protecting investment in the NHS”.

He will add: “I want to reassure taxpayers that every penny they are being asked to pay will be spent wisely.

“Our investment to offer more services at evenings and weekends, arm staff with modern technology, and improving staff retention is working.

“At the same time, cuts to wasteful spending on things like recruitment agencies saw productivity grow by 2.4% in the most recent figures – we are getting better bang for our buck.”

Health Secretary Wes Streeting during a visit to the NHS National Operations Centre in London earlier this year. Pic: PA

Mr Streeting’s speech is due to be given just hours after he became entrenched in rumours of a possible coup attempt against Sir Keir Starmer, whose poll ratings have plummeted ahead of what’s set to be a tough budget.

Mr Streeting’s spokesperson was forced to deny he was doing anything other than concentrating on the health service.

Read more from Sky News:

Russian troops in Mad Max-style video

Shamima Begum ‘should be repatriated’

He is also expected on Wednesday to give NHS leaders the go-ahead for a 50% cut to headcounts in Integrated Care Boards, which plan health services for specific regions.

They have been tasked with transforming the NHS into a neighbourhood health service – as set down in the government’s long-term plans for the NHS.

Those include abolishing NHS England, which will be brought back into the health department within two years.

Watch Wes Streeting on Mornings With Ridge And Frost from 7am on Sky News.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024