Ryanair raises passenger forecast but first quarter loss deepens

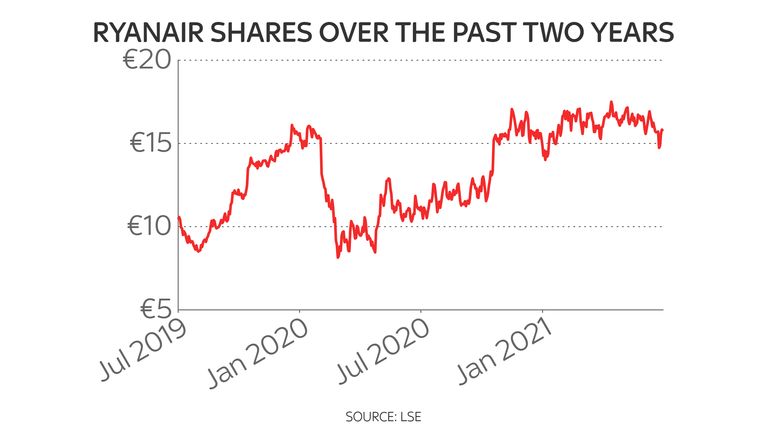

Ryanair has raised its passenger forecast following a recovery in summer bookings but reported a sharper first quarter loss, saying the coronavirus crisis “wreaked havoc” on Easter demand.

Europe’s largest airline by passenger numbers said it now expected to fly between 90 and 100 million people in its current financial year to the end of March 2022.

That was up from an earlier forecast of 80-100 million as it benefitted from a boost to summer holiday bookings and eyed a much improved winter season ahead.

It credited the improved guidance on a COVID-19 vaccine-led pick up in demand across EU nations – following in the footsteps of a recovery in the UK – though it refused to extend the range of its forecasts beyond the current year given continuing uncertainty.

Ryanair boss delivers blunt verdict on ‘pingdemic’

Ryanair said a net loss of €273m (£234m) between April and June, up from the €185m red figure in the same period last year, reflected a disastrous Easter for travel though demand had picked up through May and June.

It carried 8.1 million passengers over the first quarter – up from just 0.5 million in the same three months of 2020 as the pandemic gathered speed.

While total revenue rose to €370m, thanks in part to additional charges on passengers for things like priority boarding and seat reservations, its bottom line was hurt by a surge in operating costs to €675m.

Ryanair chief executive, Michael O’Leary, said: “COVID-19 continued to wreak havoc on our business during Q1 with most Easter flights cancelled and a slower than expected easing of EU Govt. travel restrictions into May and June.

“Significant uncertainty around travel green lists (particularly in the UK) and extreme Govt. caution in Ireland meant that Q1 bookings were close-in and at low fares.”

He added: “Following the 1st July rollout of EU digital Covid certificates (and the relaxation of the UK’s quarantine rules) for fully-vaccinated persons, our group has seen Q2 bookings recover strongly (albeit at low fares).

“We believe that FY22 traffic has improved to a range of 90m to 100m (previously guided at the lower end of an 80m to 120m passenger range) and (cautiously) expect that the likely outcome for FY22 is somewhere between a small loss and breakeven.

“This is dependent on the continued rollout of vaccines this summer and no adverse COVID variant developments.”

President Trump says he is firing a governor of the US central bank, a move seen as intensifying his bid for control over the setting of interest rates.

He posted a letter on his Truth Social platform on Monday night declaring that Lisa Cook – the first black woman to be appointed a Federal Reserve governor – was to be removed from her post on alleged mortgage fraud grounds.

She has responded, insisting he has no authority over her job and vowed to continue in the role, threatening a legal battle that could potentially go all the way to the Supreme Court.

Money latest: ‘RAC left me stranded on a busy motorway for four hours – then gave me £8’

The president‘s threat is significant as he has consistently demanded that the central bank cut interest rates to help boost the US economy. Growth has sagged since he returned to office on the back of US trade war gloom and hiring has slowed sharply in more recent months.

Mr Trump has previously directed his ire over rates at Jay Powell, the chair of the Federal Reserve, blaming him for the economic jitters and has repeatedly called for him to be fired.

The Fed, as it is known, has long been considered an institution independent from politics and question marks over that independence has previously shaken financial markets.

The dollar was hit overnight while US futures indicate a negative opening for stock markets.

Mr Powell’s term is due to end next spring and the president is expected to soon nominate his replacement.

Fed chair Jay Powell is seen in discussion with board member Lisa Cook. Pic: AP

The Fed has 12 people with a right to vote on monetary policy, which includes the setting of interest rates and some regulatory powers.

Those 12 include the seven members of the Board of Governors, of which Ms Cook is one.

Replacing her would give Trump appointees a 4-3 majority on the board.

July: Fed chair has ‘done a bad job’, says Trump

He has previously said he would only appoint Fed officials who support lower borrowing costs.

Ms Cook was appointed to the Fed’s board by then-president Joe Biden in 2022 and is the first black woman to serve as a governor.

Her nomination was opposed by most Senate Republicans at the time and was only approved, on a 50-50 vote, with the tie broken by then-vice president Kamala Harris.

It was alleged last week by a Trump appointed regulator that Ms Cook had claimed two primary residences in 2021 to get better mortgage terms.

Mortgage rates are often higher on second homes or those purchased to rent.

She responded to the president’s letter: “President Trump purported to fire me ‘for cause’ when no cause exists under the law, and he has no authority to do so,” she said in an emailed statement.

“I will not resign.”

Legal experts said it was for the White House to argue its case.

But Lev Menand, a law professor at Columbia law school, said of the situation: “This is a procedurally invalid removal under the statute.

“This is not someone convicted of a crime. This is not someone who is not carrying out their duties.”

The Fed was yet to comment.

It has held off from interest rate cuts this year, largely over fears that the president’s trade war will result in a surge of inflation due to higher import duties being passed on in the world’s largest economy.

However, Mr Powell hinted last week that a cut could now be justified due to risks of rising unemployment.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024