Ted Baker puts brave face on pandemic sales slump

Ted Baker, the formal and occasion wear retailer, has reported a slump in annual sales during the coronavirus pandemic but argued it is now better placed to navigate continuing disruption.

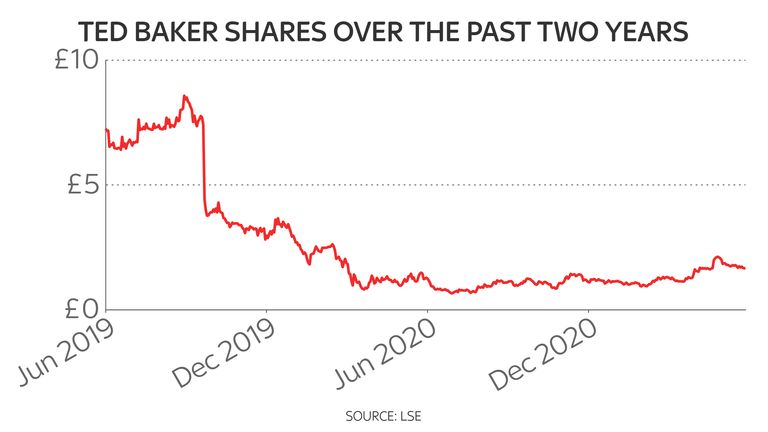

The fashion chain reported a deepening pre-tax loss of £107.7m for the year to the end of January on the back of a £77.6m sum in the previous 12 months.

The company was already in the doldrums at that time – before COVID-19 hit – as it pledged a recovery from a string of setbacks including a £58m inventory overstatement and the departure of previous chief executive and founder Ray Kelvin following misconduct allegations – claims he has denied.

Ted Baker’s founder Ray Kelvin denied claims including ‘forced hugs’ while he ran the firm

Ted Baker said on Monday that the pandemic had taken an inevitable toll on its CEO Rachel Osborne’s transformation plan, which includes a greater focus on online sales.

It revealed an underlying pre-tax loss of £59.2m for its last financial year compared to a £4.8m profit the previous year as its global store footprint fell under coronavirus trading restrictions.

Total revenue fell 44% to £352m though e-commerce sales were up 22% to £144.9m.

The company, like many rivals, had to cut jobs and raise cash during the height of the crisis as it navigated the disruption to normal life which heavily restricted demand for its prime offering.

Competitors with a focus on athleisure and casualwear have tended to do better given more people working from home and the lack of opportunities to enjoy nights out.

Ms Osborne said: “While the impact of COVID-19 is clear in our results and has amplified some of the legacy issues impacting the business, Ted Baker has responded proactively and is in a much stronger place than it was a year ago.

Ted Baker – long criticised for a lack of focus on online sales – has 521 stores and concessions worldwide

“During the period, we delivered robust cashflow generation, fixed our balance sheet, refreshed our senior leadership team and today we are upgrading our financial targets for the second time since outlining our new strategy last summer.

“Additionally, we have made good progress with our sustainability strategy, Fashioning a Better Future, including the mapping of all of our factory partners within our supply chain and significantly increasing our usage of cotton from sustainable sources to 69%.”

Shares opened positively initially but later fell back by around 1.6%.

Senior analyst at Freetrade, Dan Lane, said the results represented something of an own goal, despite the increase in e-commerce sales.

“Ted’s online presence needs an almighty boost and should have been focused on years ago.

“It finally started to get some attention as part of ‘Ted’s Formula For Growth’ but leaving it so late has meant being ill-prepared for the shift online over the year.

“It’ll be the epitome of ‘too little too late’ for a lot of beleaguered investors.”

Business

Concessions to welfare reforms to be revealed after Labour backbench rebellion forces government retreat

Changes to welfare reforms, forced on the government by rebel Labour MPs, are being revealed today ahead of a crucial vote.

The original bill restricted eligibility for the personal independence payment (PIP) and cut the health-related element of universal credit (UC).

The government, which insisted welfare costs were becoming unsustainable, was forced into a U-turn after 126 Labour backbenchers signed an amendment that would have halted the bill at its first Commons hurdle.

Explainer: What are the welfare concessions?

While the amendment is expected to be withdrawn, after changes that appeased some Labour MPs, others are still unhappy and considering backing a similar amendment to be tabled today.

Starmer defends welfare U-turn

Here are the main changes to the UC and PIP bill:

• current PIP claimants will keep their benefits; stricter eligibility requirements will only apply to new claims from November 2026

• a review of the PIP assessment, which will have input from disabled people

• existing recipients of the health-related element of UC will have their incomes protected in real terms

Work and Pensions Secretary Liz Kendall said in a statement that the legislation now aims to deliver a “fairer, more compassionate system” ahead of the second reading and vote on Tuesday.

“We must build a welfare system that provides security for those who cannot work and the right support for those who can. Too often, disabled people feel trapped, worried that if they try to work, they could lose the support they depend on.

“That is why we are taking action to remove those barriers, support disabled people to live with dignity and independence, and open routes into employment for those who want to pursue it.

“This is about delivering a fairer, more compassionate system as part of our Plan for Change which supports people to thrive, whatever their circumstances.”

Work and Pensions Secretary Liz Kendall insists welfare reforms will create ‘a fairer, more compassionate system’. Pic: PA

On Saturday, Sir Keir Starmer said fixing the UK’s welfare system was a “moral imperative”. The government claimed cuts to sickness and disability benefits would shave £5bn off the welfare bill and get more people into work.

The Resolution Foundation believes the concessions could cost as much as £3bn, while the Institute for Fiscal Studies warned that the changes make tax rises more likely.

Read more:

Starmer’s most damaging U-turn yet

Liz Kendall defends welfare retreat

👉 Click here to listen to Electoral Dysfunction on your podcast app 👈

Health Secretary Wes Streeting told Sky News that welfare bill changes have put Labour in a much better position ahead of tomorrow’s vote.

On Sunday Morning with Trevor Phillips, Mr Streeting said: “There were things that we didn’t get right, we’ve put right, and there’ll be a debate about future amendments and things, I’m sure, as it goes through in the usual way.”

Talking to Sky News about the welfare reforms, Health Secretary Wes Streeting said there were things Labour ‘didn’t get right’

On the same programme, shadow work and pensions secretary Helen Whately repeatedly refused to say whether the Conservatives would back the bill, but would review the proposals after the minister’s statement later.

“We have said that if there are more savings that actually bring the welfare bill down, if they’ll get more people into work, and if they commit to using the savings to avoid tax cuts in the autumn, which looks highly unlikely at the moment, then they have our support.”

The Liberal Democrats plan to vote against the bill and have called for the government to speed up access-to-work decisions to help people enter the workforce.

Donald Trump has said the US government has found a buyer for TikTok that he will reveal “in about two weeks”.

The president told Fox News “it’s a group of very wealthy people”, adding: “I think I’ll probably need China approval, I think President Xi will probably do it.”

TikTok was ordered last year to find a new owner for its US operation – or face a ban – after politicians said they feared sensitive data about Americans could be passed to the Chinese government.

The video app’s owner, Bytedance, has repeatedly denied such claims.

It originally had a deadline of 19 January to find a buyer – and many users were shocked when it “went dark” for a number of hours when that date came round, before later being restored.

However, President Trump has now extended the deadline several times.

The last extension was on 19 June, when he signed an executive order pushing it back to 17 September.

Mr Trump’s latest comments suggest multiple people coming together to take control of the app in the US.

Among those rumoured to be potential buyers include YouTube superstar Mr Beast, US search engine startup Perplexity AI, and Kevin O’Leary – an investor from Shark Tank (the US version of Dragons’ Den).

Bytedance said in April that it was still talking to the US government, but there were “differences on many key issues”.

It’s believed the Chinese government will have to approve any agreement.

The president said the identity of the buyer would be disclosed in about two weeks. Pic: Fox News

President Trump’s interview with Fox News also touched on the upcoming end of the pause in US tariffs on imported goods.

On April 9, he granted a 90-day reprieve for countries threatened with a tariff of more than 10% to give them time to negotiate.

Deals have already been struck with some countries, including the UK.

Read more from Sky News:

Iran could begin enriching uranium again in months – UN

Major porn sites to introduce ‘robust’ age verification in UK

The president said he didn’t think he would need to push back the 9 July deadline and that letters would be sent out imminently stating what tariff each country would face.

“We’ll look at the deficit we have – or whatever it is with the country; we’ll look at how the country treats us – are they good, are they not so good. Some countries, we don’t care – we’ll just send a high number out,” he said.

“But we’re going to be sending letters out starting pretty soon. We don’t have to meet, we have all the numbers.”

The president announced the tariffs in April, arguing they were correcting an unfair trade relationship and would return lost prosperity to US industries such as car-making.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike