Foreign governments face ban on owning British newspapers – effectively blocking Abu Dhabi-led Telegraph takeover

The government plans to ban foreign governments from owning British newspapers and magazines – effectively blocking an Abu Dhabi-led takeover of the Daily and Sunday Telegraph.

The commitment was set out in the House of Lords this afternoon in an amendment to the third reading of the Digital Markets Act, currently making its way through Parliament.

Culture minister Lord Parkinson said: “We will amend the media merger regime explicitly to rule out newspaper and periodical news magazine mergers involving ownership, influence or control by foreign states.”

He added: “Under the new measures the secretary of state would be obliged to refer media merger cases to the Competition and Markets Authority (CMA) through a new foreign state intervention notice.”

The secretary of state, the peer said, would be obliged to block deals found to contravene the CMA’s tests.

The move was revealed as the House debated an amendment, brought by Baroness Stowell but withdrawn on confirmation of the government’s plans, that had called for the banning of foreign state ownership in response to the proposed takeover of the Telegraph titles, as well as the Spectator magazine, by Redbird-IMI.

The US-Abu Dhabi joint venture is 75% owned by Sheikh Mansour, vice president of the United Arab Emirates (UAE).

The future of the Telegraph titles has been the subject of fierce debate in Conservative circles since Redbird-IMI circumvented a formal auction by repaying money owed to Lloyds Bank by former owners the Barclay family, who had put the newspapers up as security.

Former Tory leaders Lord Hague and Iain Duncan Smith opposed the takeover arguing that it was inappropriate for significant media assets to be effectively owned by a foreign state.

Scores of MPs have backed that opposition.

Culture Secretary Lucy Frazer referred the takeover to Ofcom and the CMA earlier this year on public interest grounds, effectively freezing the deal and leaving the Telegraph in limbo, the shares formally sitting with the Barclay family.

Lucy Frazer, the culture secretary, is currently reviewing reports on the takeover by the CMA and Ofcom

She is currently considering whether to ask the CMA to carry out a more in-depth “phase two” investigation that could take up to six months.

Redbird-IMI fronted by former CNN executive Jeff Zucker has consistently argued that Sheikh Mansour is investing in a personal capacity and pledged an independent editorial structure to prevent influence over content.

The government will not spell out the details of the legislation at this stage and it remains unclear what level of state investment might be permitted.

While the government’s amendment would block the 75% stake proposed in the Redbird-IMI deal, smaller minority stakes that do not grant control may be permitted.

That may leave the way clear for Redbird-IMI to restructure its deal, with Redbird Capital taking a larger stake or inviting in other investors.

Read more from business:

UK economy returns to growth

TikTok’s US future in doubt

Perkbox founders to celebrate £35m windfalls

Lord Rothermere, owner of the Daily Mail, and Rupert Murdoch’s News UK, owner of the The Times, The Sun and Sunday Times, remain interested in a stake in the Telegraph having been outmanoeuvred in the original auction.

Another potential investor is Sir Paul Marshall, a co-owner of GB News.

If Redbird-IMI is blocked or cannot restructure the deal they insist they control the shares and retain the right to manage the onward sale of the titles. They are likely to face opposition from the Barclay family, who may try and retain control by raising fresh funding.

The proposed legislation may send a mixed message to overseas investors, particularly the UAE, which the government has enthusiastically courted as a partner in key industries.

The UAE has pumped money into numerous high-profile projects as part of a £10bn five-year investment programme, including wind farms and life sciences, and has been approached about a potential stake in the Sizewell C nuclear power station.

How soon is too soon?

That’s the question exercising members of the Bank of England‘s monetary policy committee (MPC) at the moment. All nine members know that interest rates, currently at 5.25%, will have to be cut in the coming months.

After all, high interest rates represent a brake on the economy and it’s becoming clear that keeping the brake pedal down is causing economic pain.

Money latest: Reaction as Bank of England holds off on rate cut

Unemployment is beginning to rise; the strength of consumer demand is dropping and, most of all, inflation is coming down too.

For Bank insiders, the fact that the rate at which the consumer price index is rising each year is about (at least according to their forecasts) to hit 2% is a mark of success.

Not long ago, as prices rose at the fastest rate in decades, many in the City wondered whether the Bank might have lost control of inflation – which it is supposed to keep as close as possible to 2%.

While the indicator’s fall is partly down to the volatility of energy prices (having been the main force lifting prices in recent years, they are now the main force depressing them), what gives the Bank’s policymakers hope is that while CPI inflation is expected to bounce back slightly in the coming months, their forecast suggests it will not exceed 3%.

The upshot is that inside the Bank there are some who are now whispering quietly that they might have succeeded – inflation might have been tamed.

But that brings us back to that question: if inflation is tamed then there’s no need to have interest rates so high, so how soon should they be cut?

Complicating factors is what’s happening on the other side of the Atlantic, where the Federal Reserve, America’s central bank, has committed something of a U-turn.

Higher US rates would tend to weigh on the pound, making imports bought in dollars more expensive. Pic: Reuters

Having guided investors and economists a few years ago that an interest rate cut was coming soon, the Fed chair, Jerome Powell, has more lately hinted that no cut was coming anytime soon.

And since America usually leads the way on interest rates, that raises an unnerving question: can the UK really begin cutting rates so long before the Federal Reserve?

The Bank’s internal assessment is quite simply that the British economy is in a very different place to America. The US is growing very strongly indeed, partly thanks to large federal spending programmes pumping cash into green tech and semiconductor manufacturing.

There is nothing analogous in the UK, whose economy is expected to grow by 0.9% over the next 12 months or so.

Keep up with all the latest news from the UK and around the world by following Sky News

That’s an upgrade on the previous 0.6% forecast, but is only a fraction of the 2%+ growth enjoyed in the US.

In the coming weeks, we’re expecting an unusually important set of economic numbers. Inflation data for April is expected to show a big fall, down to 2%. There are some jobs data and, of course, tomorrow we learn whether the UK has bounced out of its current recession (it almost certainly has).

In the end, this data is what will determine whether the MPC is bold enough to cut rates in June or in August (or, if the data shows an unexpected increase in inflation, to put those cuts off for longer).

So it’s a waiting game. But it looks like there’s not that much longer to wait.

The Bank of England has edged closer to a cut in interest rates, with another member of its nine-person Monetary Policy Committee (MPC) voting for lower borrowing costs this month.

While the MPC voted 7-2 to leave UK interest rates on hold at 5.25%, the change in the vote will be seen as a further sign that they could be coming down soon – perhaps as soon as next month.

Money latest: Reaction to interest rates announcement

Forecasts

Alongside its rate decision, the Bank published new forecasts for the UK economy, which show that gross domestic product (GDP) is projected to be stronger this year and unemployment and inflation rates lower than previously expected.

It said that the CPI rate of inflation was likely to drop to its 2% target imminently – though it would bounce a little higher afterwards.

‘Optimistic things are moving in the right direction’

Governor Andrew Bailey said: “We’ve had encouraging news on inflation and we think it will fall close to our 2% target in the next couple of months. We need to see more evidence that inflation will stay low before we can cut interest rates.

“I’m optimistic that things are moving in the right direction.”

The documents released today are likely to reinforce the view among economists that even though the US central bank, the Federal Reserve, has hinted it won’t cut interest rates anytime soon, the Bank is likely to cut them this summer.

The main debate among investors is when that cut will happen: as of this morning they were betting the first quarter percentage point cut would come in August, though some think it could be as soon as next month.

Higher interest rates – who was to blame?

Those who try to construe likely future decisions based on the voting patterns on the committee will see significance in the fact that Dave Ramsden, one of the Bank’s deputy governors, has joined Swati Dhingra in voting for lower interest rates.

Often the change in the vote of a senior internal MPC member – as opposed to one of the four external MPC members (of which Ms Dhingra is one) – signifies that the rest of the committee may soon follow suit.

The critical line from the minutes of today’s decision reads that the MPC “would consider forthcoming data releases and how these informed the assessment that the risks from inflation persistence were receding.”

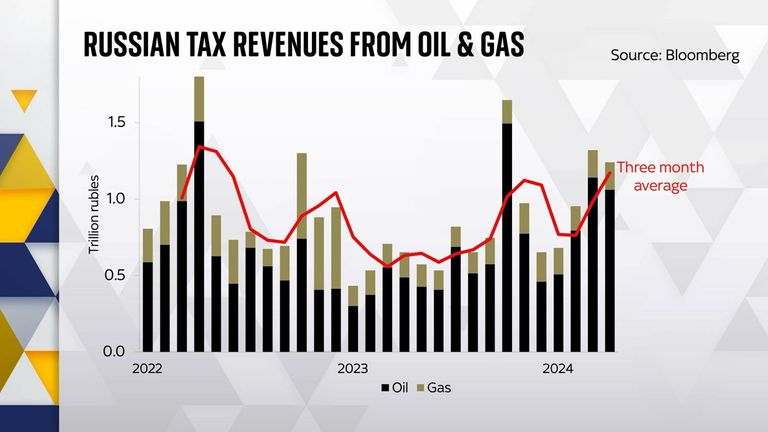

The Russian state has been making more money from its oil and gas industry in the past three months than in any comparable period since the early days of the Ukraine invasion, it has emerged.

The figures underline that despite the imposition of various sanctions on fossil fuel exports from Russia since February 2022, the country is still making significant sums from them. This is in part because rather than preventing Russia from exporting oil, gas and coal, they have simply changed the geography of the global fossil fuels business.

In the three months to April, Russia made a monthly average of 1.2 trillion rubles (£10.4bn) from its oil and gas revenues, according to Sky analysis of figures collected by Bloomberg.

That is the highest three-month average since April 2022.

It comes amid elevated oil prices and concerns that sanctions on Russia are failing to prevent the country earning money and waging war on Ukraine.

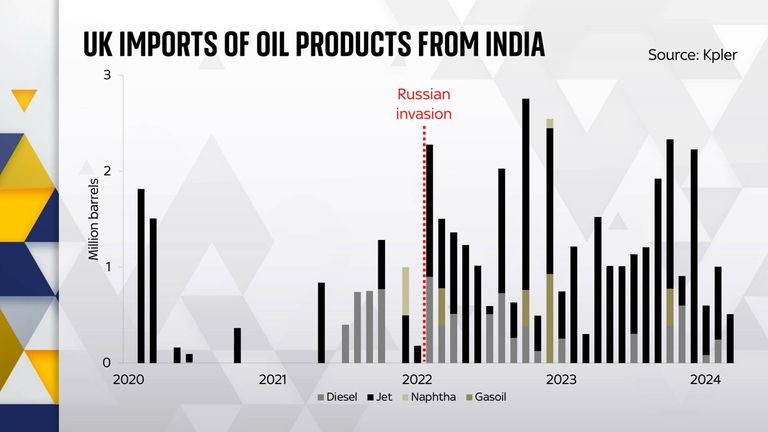

Before the invasion of Ukraine, the world’s biggest recipients of Russian oil experts were the European Union, the US and China. Since then, the UK, US and EU have banned the import of crude oil or refined products from Russia.

G7 nations have also introduced a price cap which aims to prevent any Western companies – from shipping firms to insurers – from assisting with any Russian oil exports for anything more than $60 a barrel.

However, Russia continues to export just as much oil as it did before the invasion of Ukraine and the imposition of the price cap.

Sanctions experts say the price cap has been a qualified success, since it has slightly reduced the potential revenues enjoyed by the Kremlin, if it intends to ship that oil via most commercial ships. In response, Russia is reported to have built up a so-called “dark fleet” of ships carrying Russian oil without obeying those sanctions.

The top three destinations for Russian oil are now China, India and Turkey. The UK now imports considerably more oil and oil products from the Middle East than before, making it more reliant on the Gulf.

However, Russian fossil fuel molecules are still being exported to the UK, albeit indirectly, because the sanctions imposed by western nations do not cover oil products refined elsewhere.

The upshot is that Indian refineries are importing a record amount of oil from Russia, and Britain is importing a record amount of oil from Indian refineries – up by 176% since the invasion of Ukraine.

At least some Russian oil still powers the cars in Britain and the planes refilling in British airports, but because it is impossible to trace the fossil fuels molecule by molecule, it is hard to know precisely how much.

-

Sports2 years ago

Sports2 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Environment12 months ago

Environment12 months agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports3 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports6 months ago

Sports6 months agoGame 1 of WS least-watched in recorded history

-

Sports1 month ago

Sports1 month agoStory injured on diving stop, exits Red Sox game

-

Environment1 year ago

Environment1 year agoGame-changing Lectric XPedition launched as affordable electric cargo bike

-

Environment1 year ago

Environment1 year agoTesla advances Powerwall pilot project with German electric company